2.5 — Precision and Diagnostics

ECON 480 • Econometrics • Fall 2022

Dr. Ryan Safner

Associate Professor of Economics

safner@hood.edu

ryansafner/metricsF22

metricsF22.classes.ryansafner.com

Contents

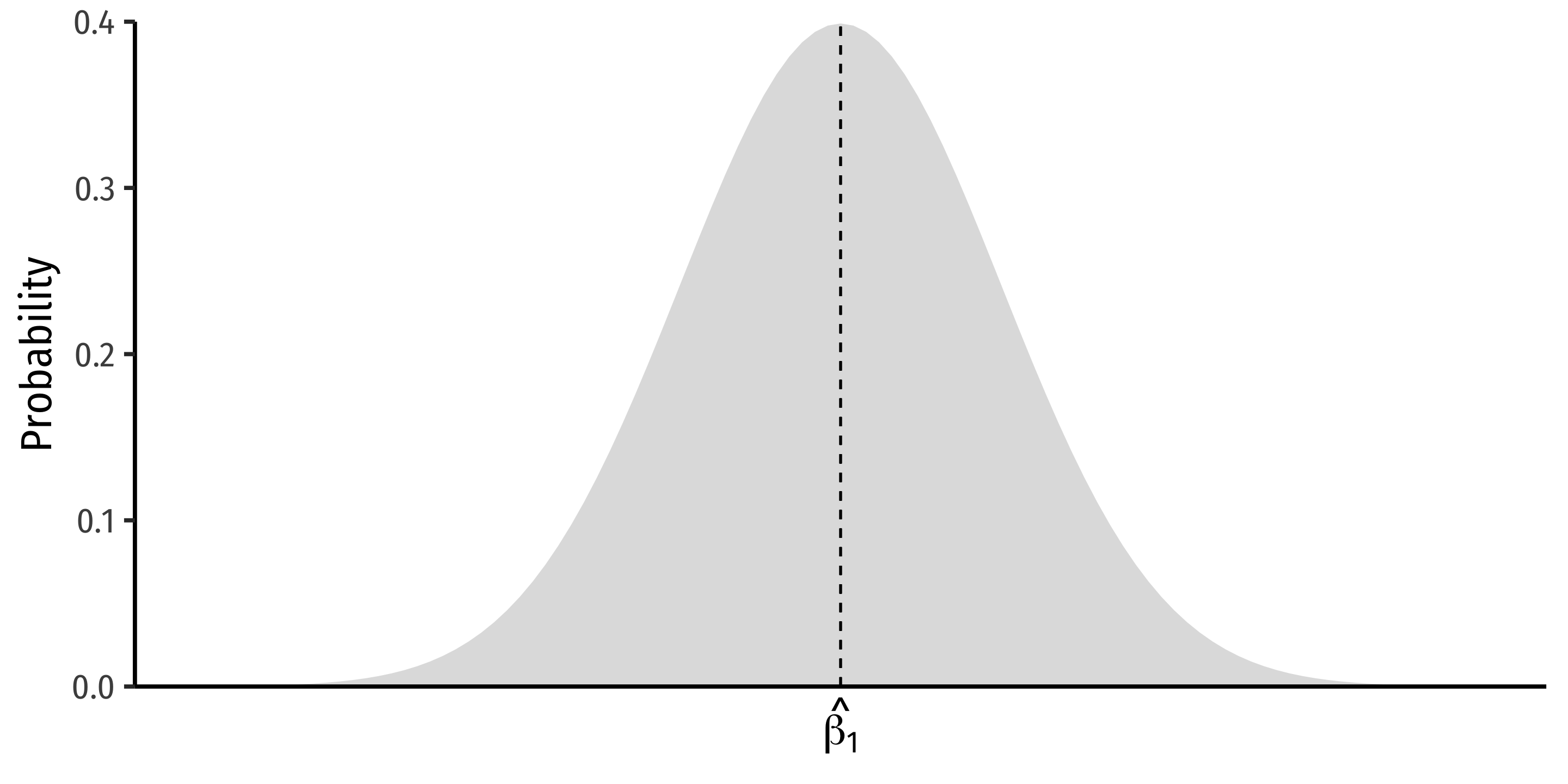

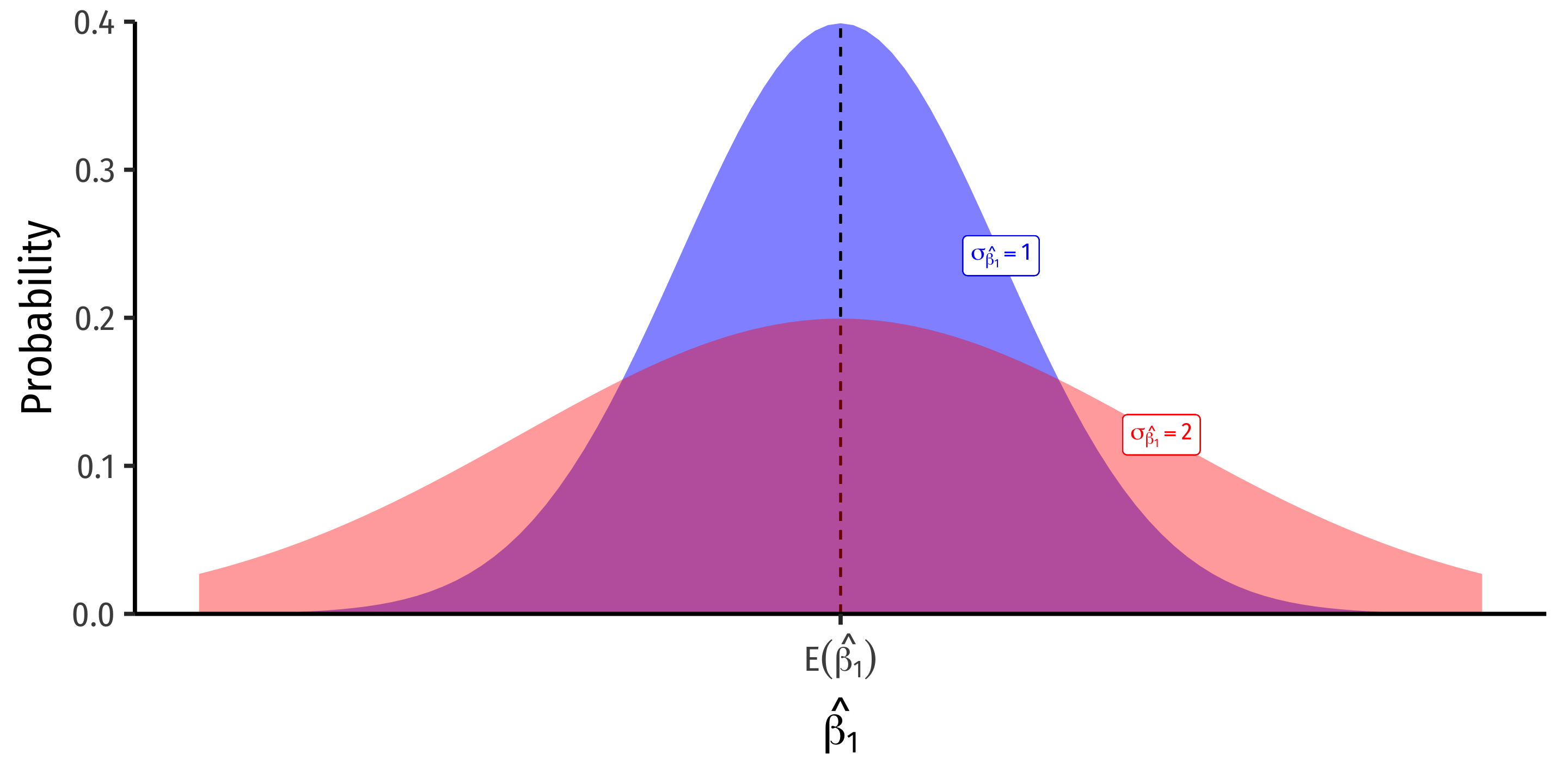

The Sampling Distribution of ^β1

^β1∼N(E[^β1],σ^β1)

The Sampling Distribution of ^β1

^β1∼N(E[^β1],σ^β1)

- Center1 of the distribution: E[^β1] (last class)

The Sampling Distribution of ^β1

^β1∼N(E[^β1],σ^β1)

Center1 of the distribution: E[^β1] (last class)

Precision or uncertainty of the estimate (today)

- Variance σ2ˆβ1

- Standard error2 σˆβ1=√var(ˆβ1)

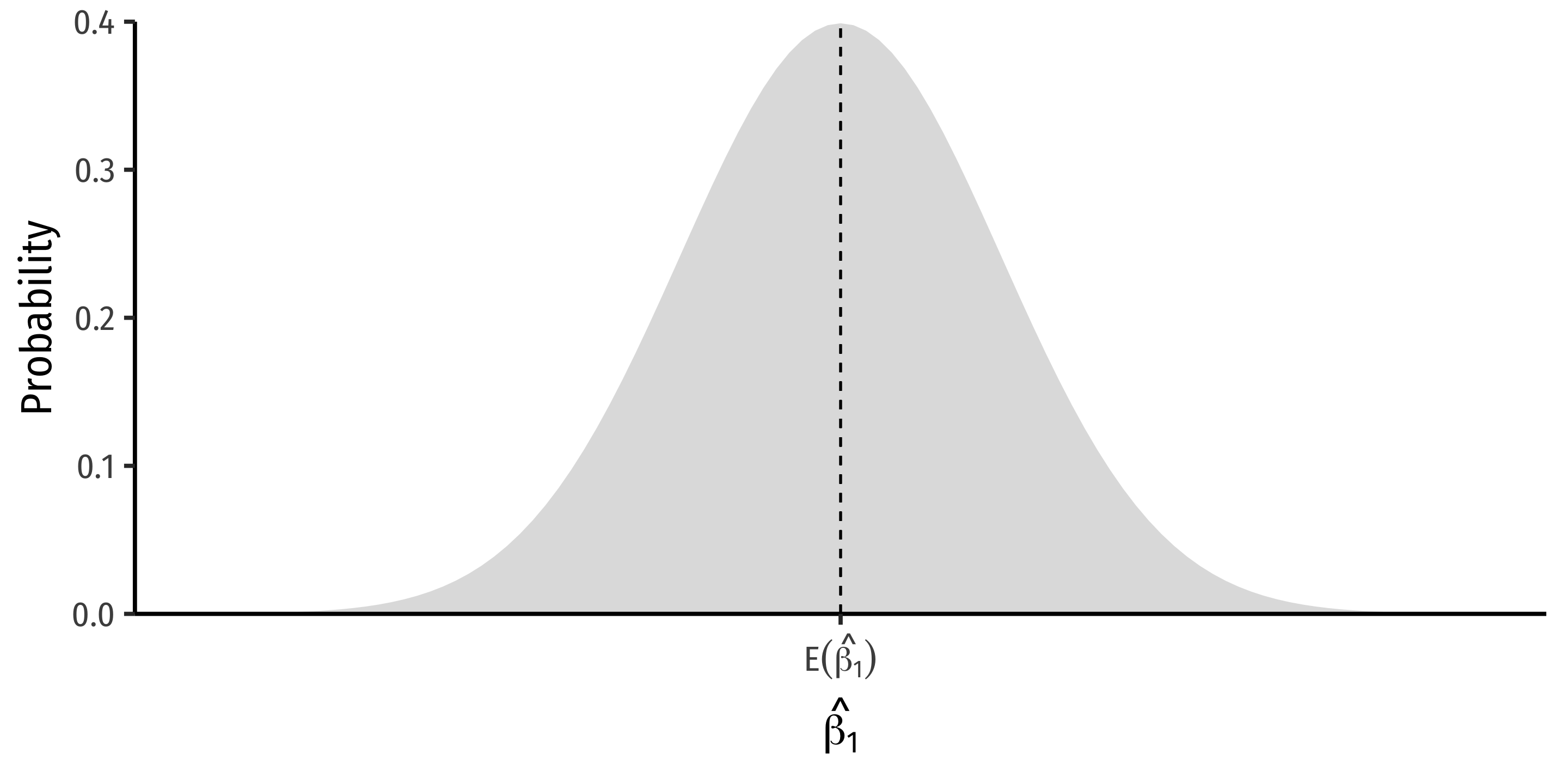

The Sampling Distribution of ^β1

^β1∼N(E[^β1],σ^β1)

Center1 of the distribution: E[^β1] (last class)

Precision or uncertainty of the estimate (today)

- Variance σ2ˆβ1

- Standard error2 σˆβ1=√var(ˆβ1)

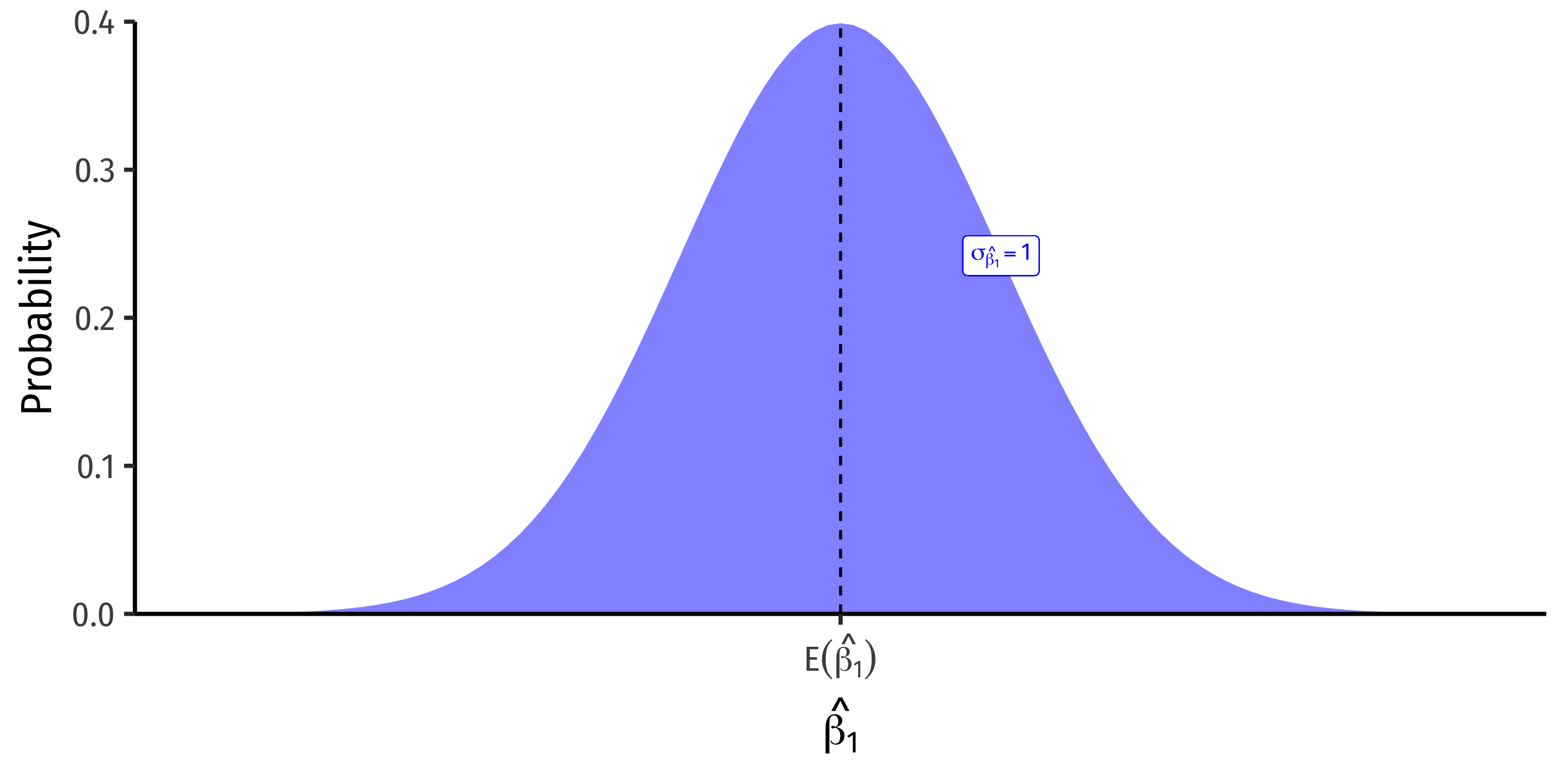

Variation in ˆβ1

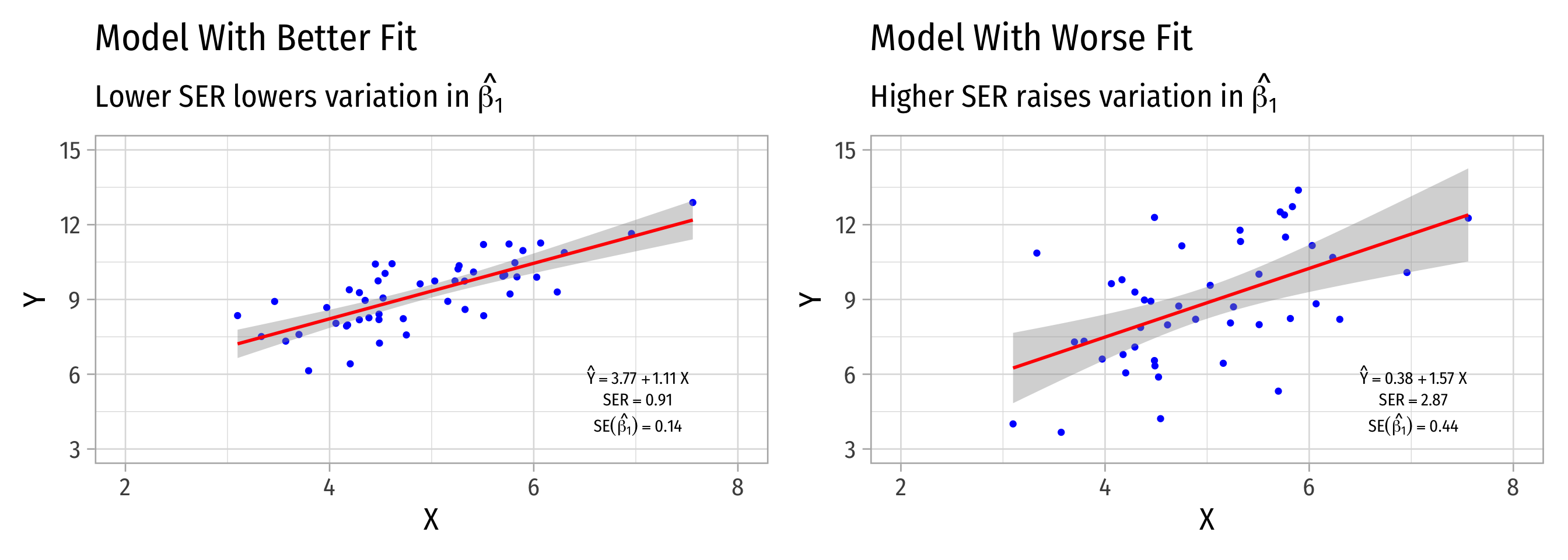

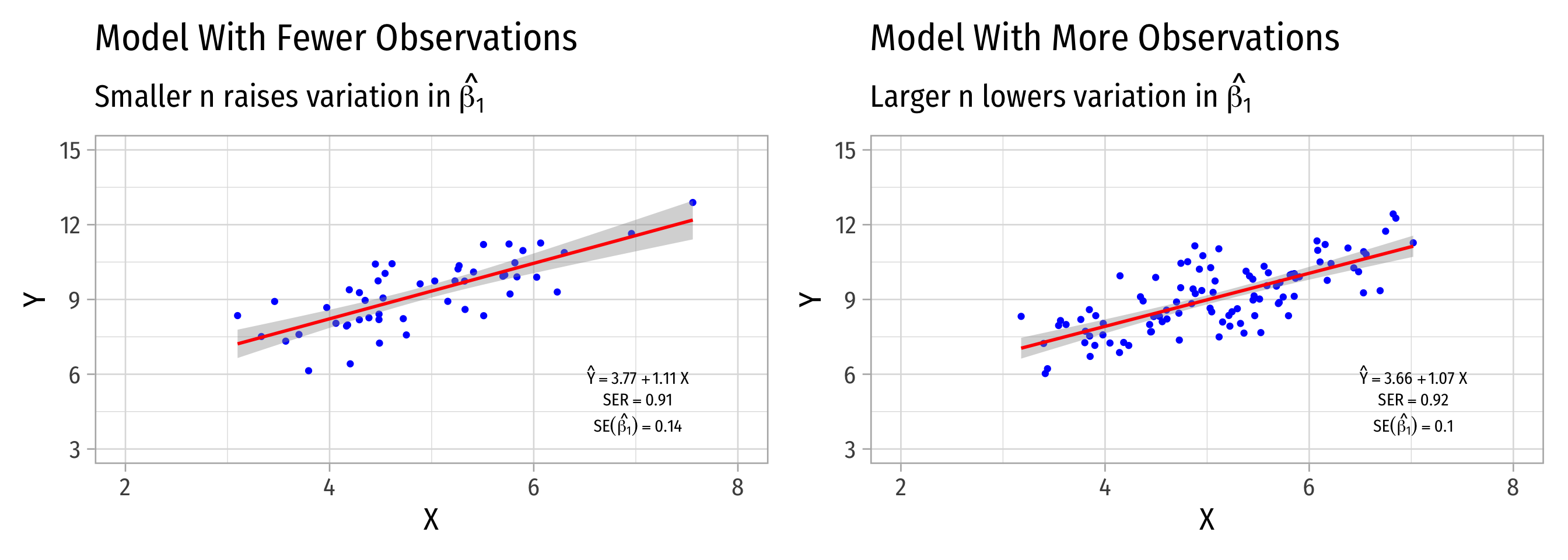

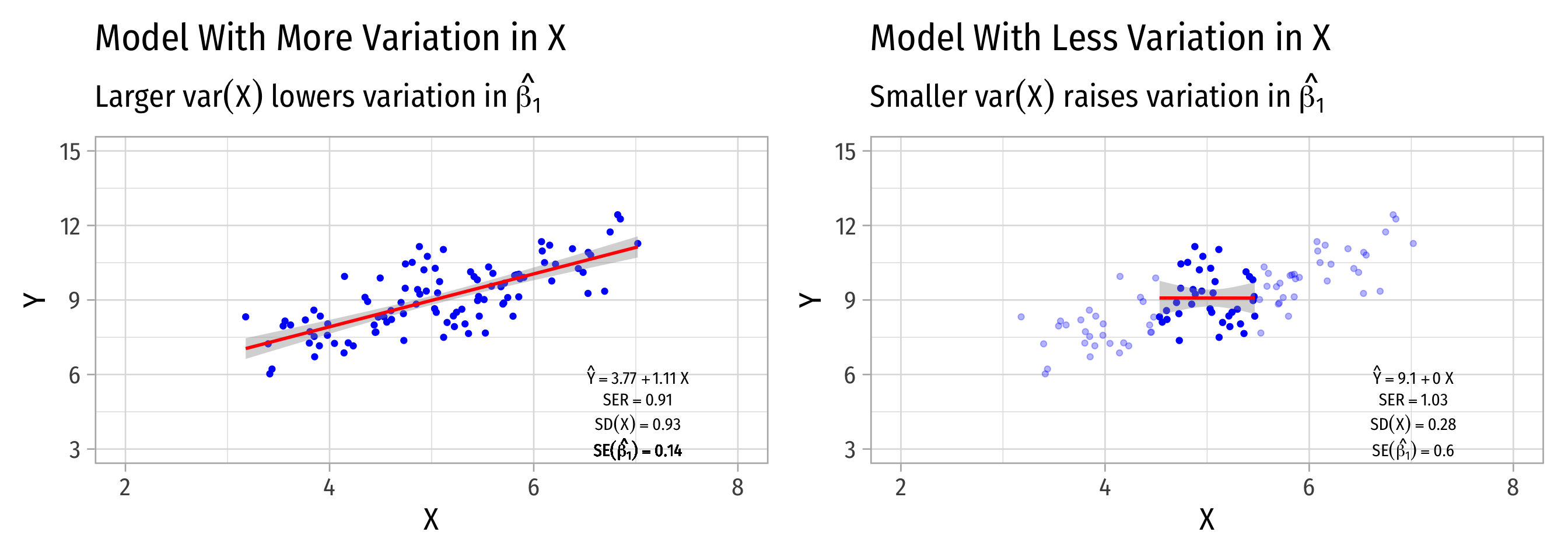

What Affects Variation in ^β1

var(^β1)=(SER)2n×var(X)

se(^β1)=√var(^β1)=SER√n×sd(X)

- Variation in ^β1 is affected by 3 things:

- Goodness of fit of the model (SER)1

- Larger SER → larger var(^β1)

- Sample size, n

- Larger n → smaller var(^β1)

- Variance of X

- Larger var(X) → smaller var(^β1)

Variation in ^β1: Goodness of Fit

Variation in ^β1: Sample Size

Variation in ^β1: Variation in X

Presenting Regression Results

Our Class Size Regression

Call:

lm(formula = testscr ~ str, data = ca_school)

Residuals:

Min 1Q Median 3Q Max

-47.727 -14.251 0.483 12.822 48.540

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 698.9330 9.4675 73.825 < 2e-16 ***

str -2.2798 0.4798 -4.751 2.78e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 18.58 on 418 degrees of freedom

Multiple R-squared: 0.05124, Adjusted R-squared: 0.04897

F-statistic: 22.58 on 1 and 418 DF, p-value: 2.783e-06- How can we present all of this information in a tidy way?

Our Class Size Regression

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| (Intercept) | 698.932952 | 9.4674914 | 73.824514 | 0.0e+00 |

| str | -2.279808 | 0.4798256 | -4.751327 | 2.8e-06 |

- Better (?), but still not how you see regressions reported in reports…especially when you have many regression models!

Regression Tables

- Professional journals and papers often have a regression table, including:

- Estimates of ^β0 and ^β1

- Standard errors of ^β0 and ^β1 (often below, in parentheses)

- Indications of statistical significance (often with asterisks)

- Measures of regression fit: R2, SER, etc

- Later: multiple rows & columns for multiple variables & models

| Test Score | |

|---|---|

| Constant | 698.93*** |

| (9.47) | |

| STR | −2.28*** |

| (0.48) | |

| n | 420 |

| R2 | 0.05 |

| SER | 18.54 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

Regression Output Tables

- A number of packages (and documentation/guides) that will make nice regression output tables for you:

- modelsummary

- stargazer (and a good cheat sheet)

- huxtable

| Test Score | |

|---|---|

| Constant | 698.93*** |

| (9.47) | |

| STR | −2.28*** |

| (0.48) | |

| n | 420 |

| R2 | 0.05 |

| SER | 18.54 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

Using modelsummary I

You will need to first

install.packages("modelsummary")Load with

library(modelsummary)Command:

modelsummary()Main argument is the name of your

lmregression objectDefault output is fine, but often we want to customize a bit!

| Model 1 | |

|---|---|

| (Intercept) | 698.933 |

| (9.467) | |

| str | −2.280 |

| (0.480) | |

| Num.Obs. | 420 |

| R2 | 0.051 |

| R2 Adj. | 0.049 |

| AIC | 3650.5 |

| BIC | 3662.6 |

| F | 22.575 |

| RMSE | 18.54 |

Using modelsummary II

- Whole command is

modelsummary(), everything will go in()

models, alist()of models to use, can give a name to each model, will show up as column title in table

Using modelsummary III

- Whole command is

modelsummary(), everything will go in()

gof_map: alist()of goodness of fit statistics, can customize what you want to include/exclude, what you want to label them in the table…a bit advanced, here’s what I like:

- Other minor options (combine with commas):

fmt = 2, # round to 2 decimals

output = "html" # depending on type of document creating; pdf would be "latex"

escape = FALSE # allows formatting of things like <sup>2</sup>

stars = c('*' = .1, '**' = .05, '***' = 0.01) # show significance levels if set to true, I don't like the defaults so I set my ownUsing modelsummary IV

modelsummary(models = list("Test Score" = school_reg),

fmt = 2, # round to 2 decimals

output = "html",

coef_rename = c("(Intercept)" = "Constant",

"str" = "STR"),

gof_map = list(

list("raw" = "nobs", "clean" = "n", "fmt" = 0),

list("raw" = "r.squared", "clean" = "R<sup>2</sup>", "fmt" = 2),

#list("raw" = "adj.r.squared", "clean" = "Adj. R<sup>2</sup>", "fmt" = 2),

list("raw" = "rmse", "clean" = "SER", "fmt" = 2)

),

escape = FALSE,

stars = c('*' = .1, '**' = .05, '***' = 0.01)

)| Test Score | |

|---|---|

| Constant | 698.93*** |

| (9.47) | |

| STR | −2.28*** |

| (0.48) | |

| n | 420 |

| R2 | 0.05 |

| SER | 18.54 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

modelplot() in modelsummary

Also nice about the modelsummary package is the command modelplot()

modelplot() in modelsummary

Also nice about the modelsummary package is the command modelplot()

Though You Could Make It Yourself in ggplot

- Use the

conf.lowandconf.high(from atidyregression) asxminandxmaxaesthetics insidegeom_errorbarh().

Diagnostics About Regression

Diagnostics: Residuals I

We often look at the residuals of a regression to get more insight about its goodness of fit and its bias

Recall

broom’saugmentcreates some useful new variables.fittedare fitted (predicted) values from model, i.e. ˆYi.residare residuals (errors) from model, i.e. ˆui

Diagnostics: Residuals II

- Often a good idea to store in a new object (so we can make some plots)

| testscr | str | .fitted | .resid | .hat | .sigma | .cooksd | .std.resid |

|---|---|---|---|---|---|---|---|

| 690.80 | 17.88991 | 658.1474 | 32.65260 | 0.0044244 | 18.53408 | 0.0068925 | 1.7612148 |

| 661.20 | 21.52466 | 649.8608 | 11.33917 | 0.0047485 | 18.59490 | 0.0008927 | 0.6117112 |

| 643.60 | 18.69723 | 656.3069 | -12.70689 | 0.0029742 | 18.59279 | 0.0006996 | -0.6848850 |

| 647.70 | 17.35714 | 659.3620 | -11.66198 | 0.0058575 | 18.59441 | 0.0011673 | -0.6294767 |

| 640.85 | 18.67133 | 656.3659 | -15.51592 | 0.0030072 | 18.58766 | 0.0010548 | -0.8363024 |

| 605.55 | 21.40625 | 650.1308 | -44.58076 | 0.0044603 | 18.47411 | 0.0129531 | -2.4046387 |

Recall: Assumptions about Errors

- We make 4 critical assumptions about u:

- The expected value of the errors is 0

E[u]=0

- The variance of the errors over X is constant:

var(u|X)=σ2u

- Errors are not correlated across observations:

cor(ui,uj)=0∀i≠j

- There is no correlation between X and the error term:

cor(X,u)=0 or E[u|X]=0

Assumptions 1 and 2: Errors are i.i.d.

- Assumptions 1 and 2 assume that errors are coming from the same (normal) distribution

u∼N(0,σu)

- Assumption 1: E[u]=0

- Assumption 2: sd(u|X)=σu

- virtually always unknown…

- We often can visually check by plotting a histogram of u

Plotting a Histogram of Residuals

Checking the Distribution of Residuals

Call:

lm(formula = testscr ~ str, data = ca_school)

Residuals:

Min 1Q Median 3Q Max

-47.727 -14.251 0.483 12.822 48.540

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 698.9330 9.4675 73.825 < 2e-16 ***

str -2.2798 0.4798 -4.751 2.78e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 18.58 on 418 degrees of freedom

Multiple R-squared: 0.05124, Adjusted R-squared: 0.04897

F-statistic: 22.58 on 1 and 418 DF, p-value: 2.783e-06Residual Plot

- We often plot a residual plot to see any odd patterns about residuals

- x-axis are ˆYi values (

.fitted) - y-axis are ui values (

.resid)

- x-axis are ˆYi values (

ggplot(data = aug_reg)+

aes(x = .fitted,

y = .resid)+

geom_point(color = "blue")+

geom_hline(aes(yintercept = 0), color = "red")+

labs(x = expression(paste("Predicted Test Score,", hat(y)[i])),

y = expression(paste("Residual, ", hat(u)[i])))+

theme_light(base_family = "Fira Sans Condensed",

base_size = 20)Heteroskedasticity

Homoskedasticity

- “Homoskedasticity:” variance of the residuals over X is constant, written:

var(u|X)=σ2u

- Knowing the value of X does not affect the variance (spread) of the errors

Heteroskedasticity I

- “Heteroskedasticity:” variance of the residuals over X is NOT constant:

var(u|X)≠σ2u

This does not cause ^β1 to be biased, but it does cause the standard error of ^β1 to be incorrect

This does cause a problem for inference!

- Specifically, it will make se(ˆβ1) wrong (often too small)1

Heteroskedasticity II

- Recall the formula for the standard error of ^β1:

se(^β1)=√var(^β1)=SER√n×sd(X)

- This assumes homoskedasticity (Assumption 2)

Heteroskedasticity III

- A better formula for estimating standard errors that are robust to heteroskedasticity (called “robust standard errors”):

se(^β1)=√n∑i=1(Xi−ˉX)2ˆu2[n∑i=1(Xi−ˉX)2]2

- Don’t learn formula, do learn what heteroskedasticity is and how it affects our model!

Visualizing Heteroskedasticity I

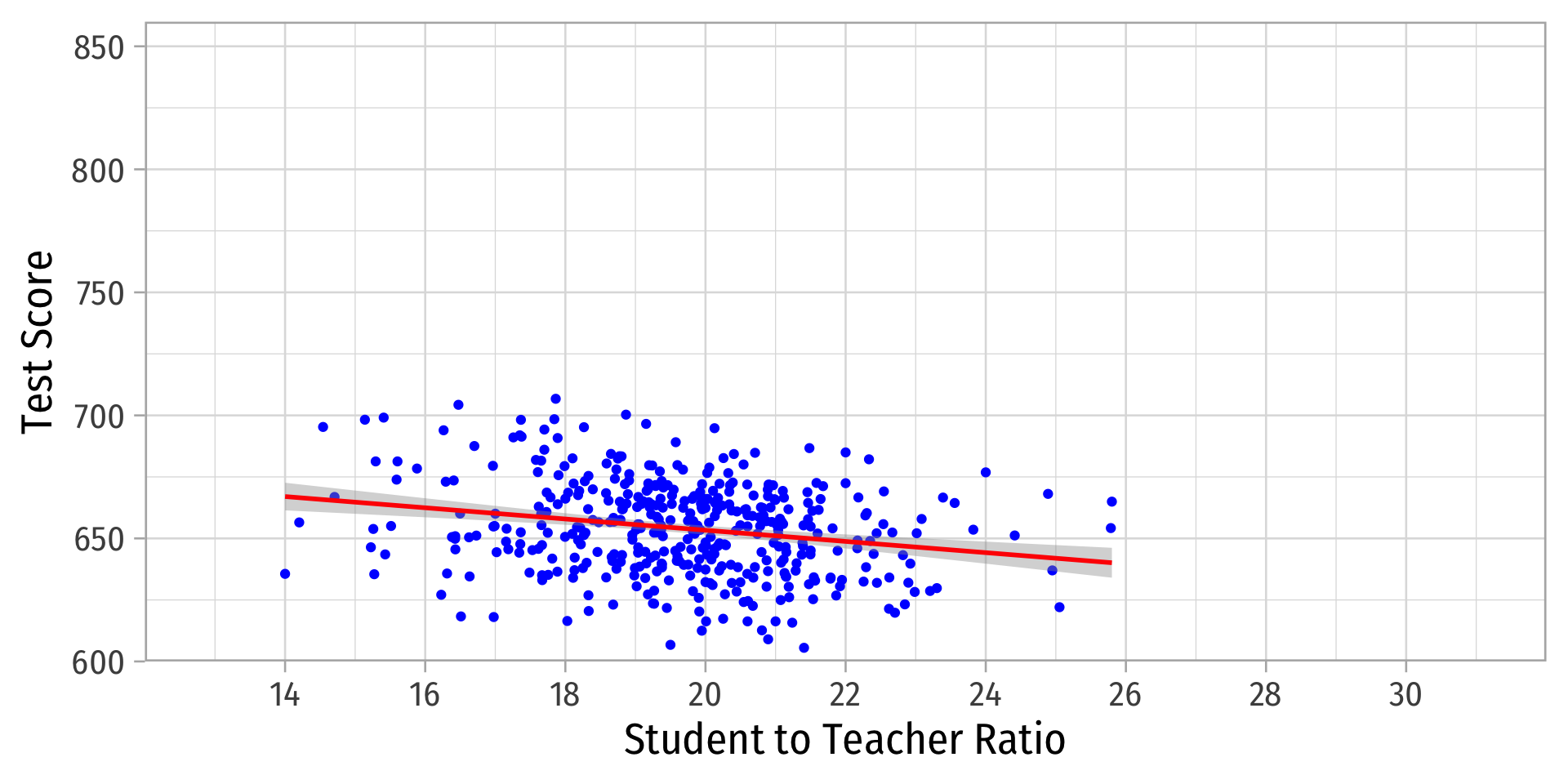

Our original scatterplot with regression line

Does the spread of the errors change over different values of str?

- No: homoskedastic

- Yes: heteroskedastic

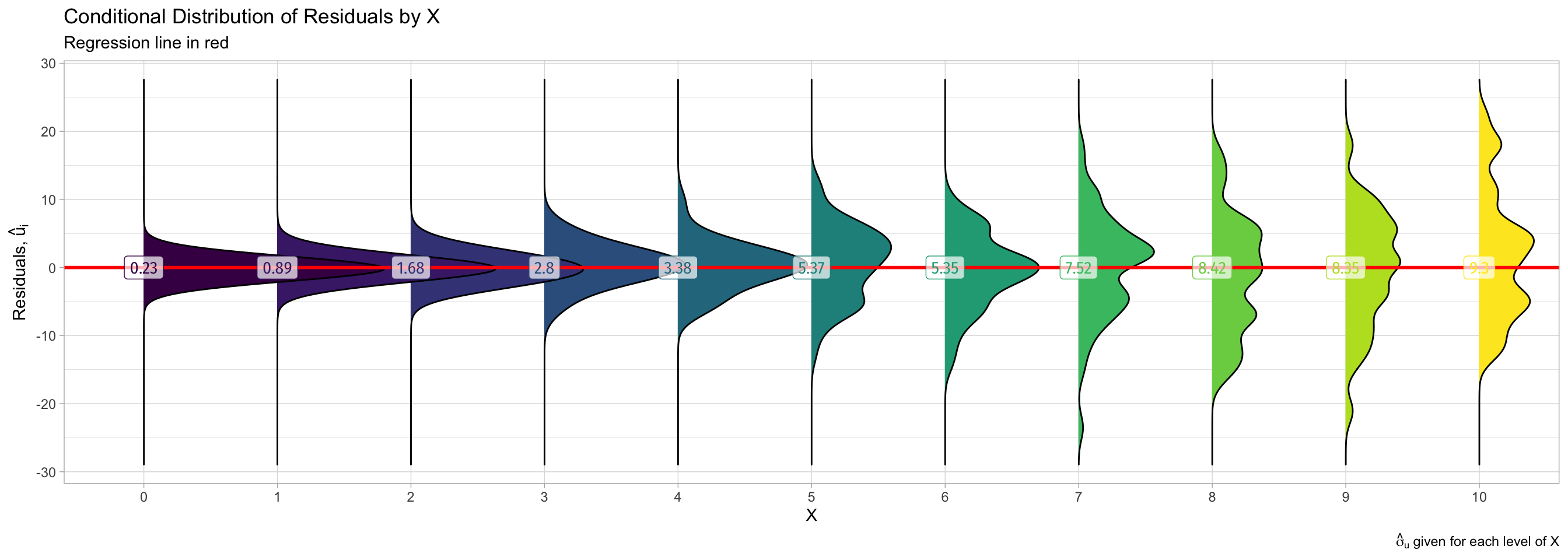

Visualizing Heteroskedasticity

- Notice the distribution of ˆu, changes for different values of STR, and σˆu is not constant

More Obvious Heteroskedasticity

- Visual cue: data is “fan-shaped”

- Data points are closer to line in some areas

- Data points are more spread from line in other areas

More Obvious Heteroskedasticity

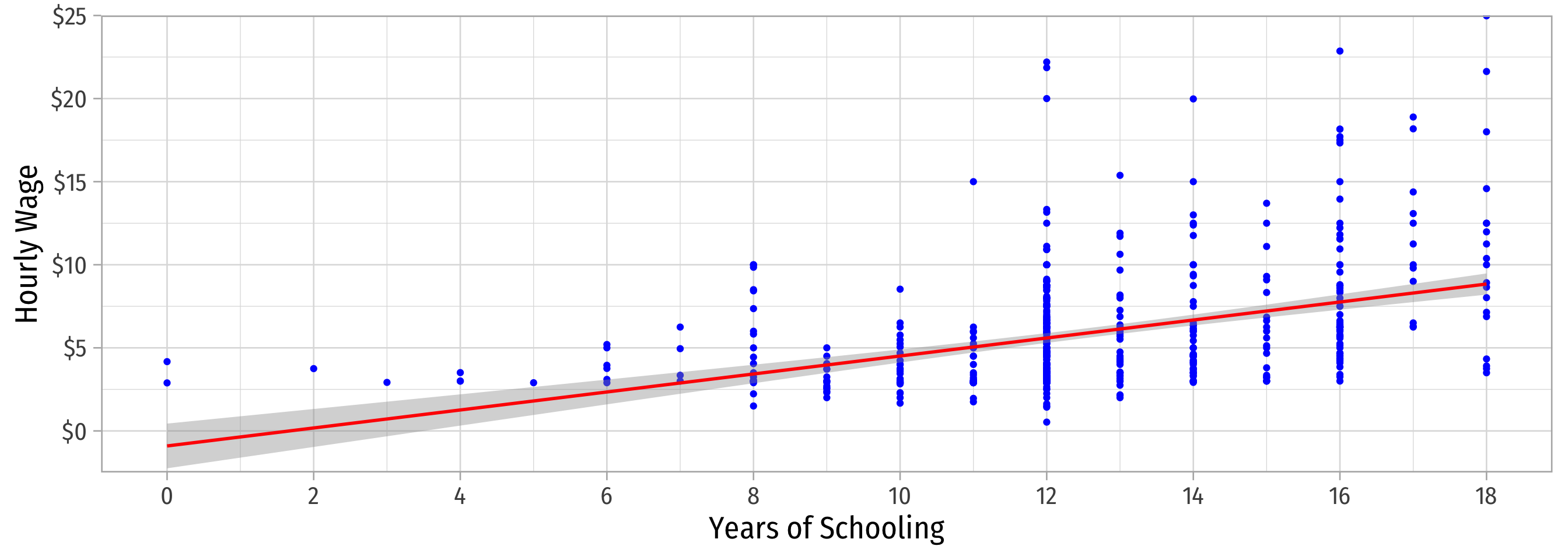

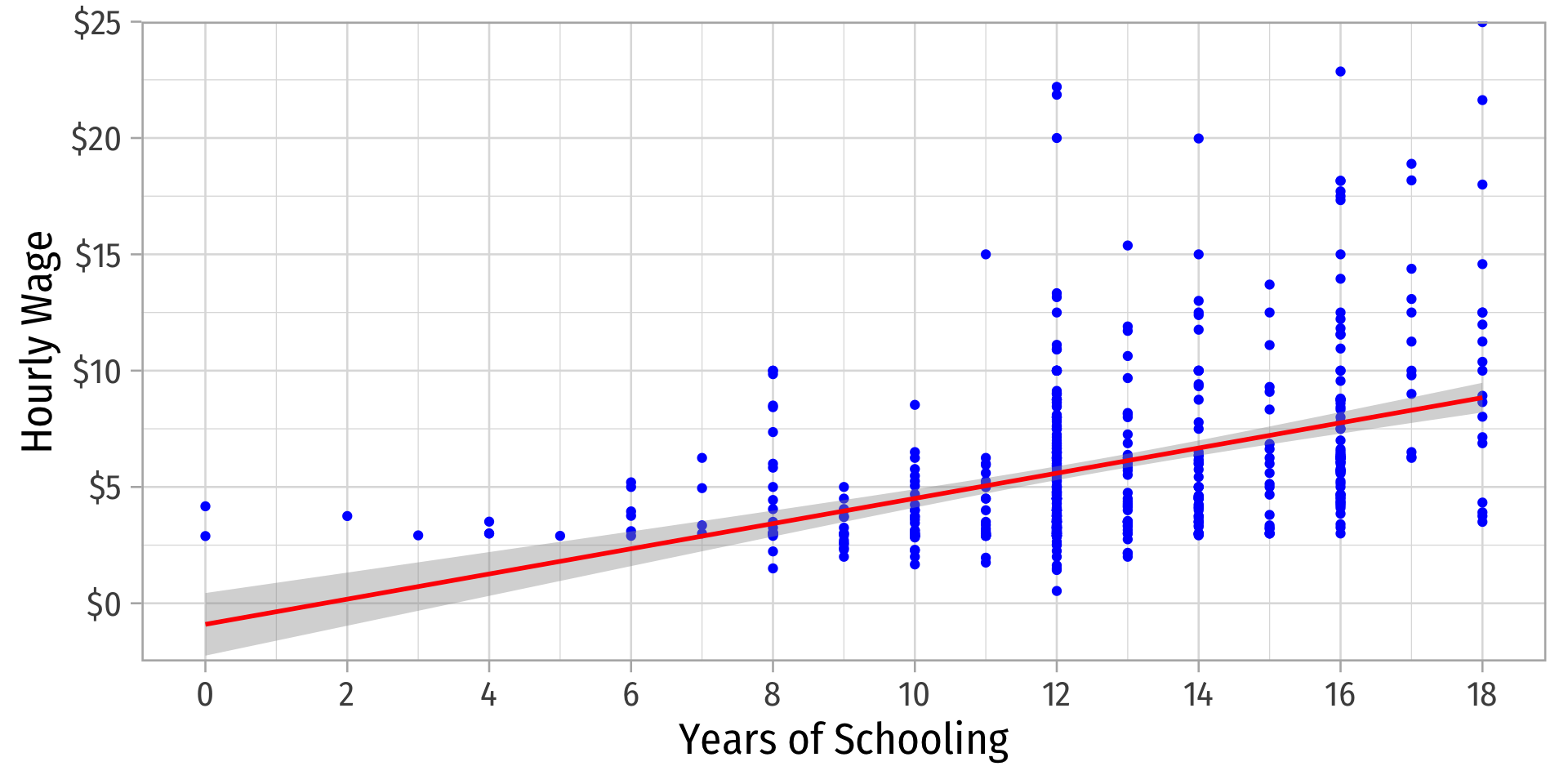

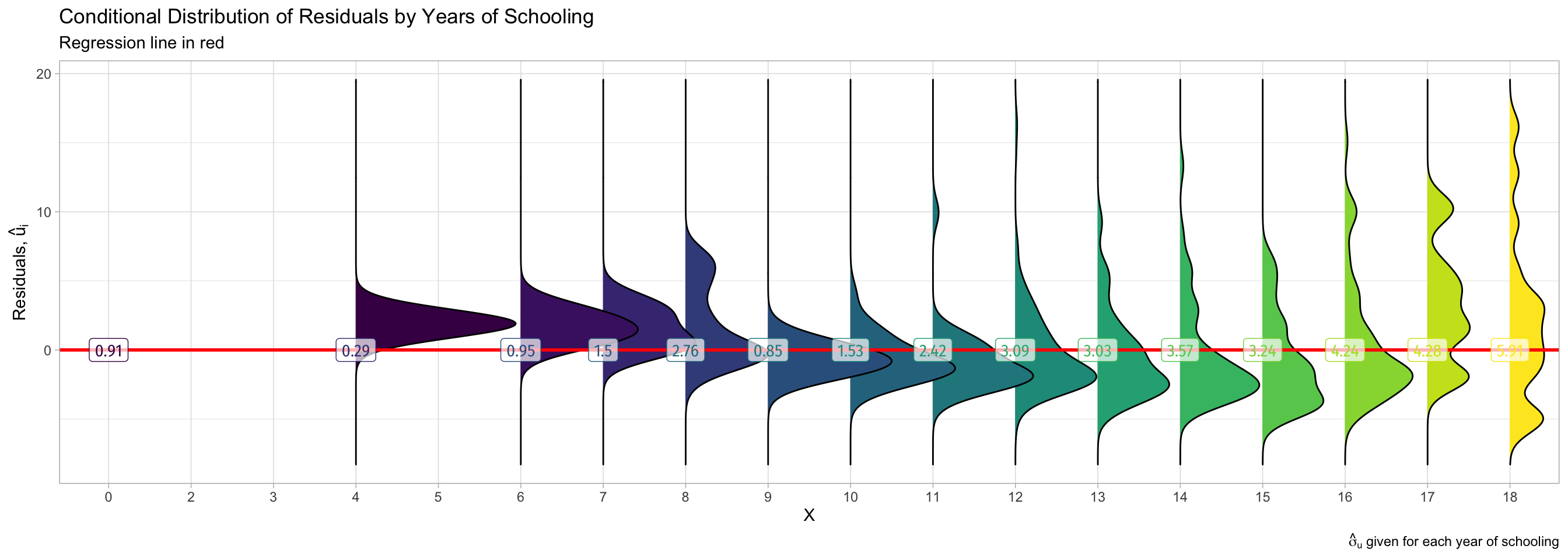

What Might Cause Heteroskedastic Errors?

wagei=β0+β1educi+ui

What Might Cause Heteroskedastic Errors?

wagei=β0+β1educi+ui

What Might Cause Heteroskedastic Errors?

wagei=β0+β1educi+ui

| Wage | |

|---|---|

| Intercept | −0.90 |

| (0.68) | |

| Years of Schooling | 0.54*** |

| (0.05) | |

| n | 526 |

| R2 | 0.16 |

| SER | 3.37 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

What Might Cause Heteroskedastic Errors?

Detecting Heteroskedasticity I

- Several tests to check if data is heteroskedastic

- One common test is Breusch-Pagan test

- Can use the

lmtestpackage’s functionbptest()- H0: homoskedastic1

- If p-value < 0.05, reject H0⟹ heteroskedastic

studentized Breusch-Pagan test

data: .

BP = 5.7936, df = 1, p-value = 0.01608- Since p<0.05, can reject H0 that errors are homoskedastic and conclude they are heteroskedastic

How About the Wages Regression?

Fixing Heteroskedasticity I

- Heteroskedasticity is easy to fix with software that can calculate robust standard errors (using the more complicated formula above)

- Easiest method is to use

estimatrpackagelm_robust()command (instead oflm) to run regression- set

se_type = "stata"to calculate robust SEs using the formula above1

Fixing Heteroskedasticity II

Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper

(Intercept) 698.932952 10.3643599 67.436191 9.486678e-227 678.560192 719.305713

str -2.279808 0.5194892 -4.388557 1.446737e-05 -3.300945 -1.258671

DF

(Intercept) 418

str 418

Call:

lm_robust(formula = testscr ~ str, data = ca_school, se_type = "stata")

Standard error type: HC1

Coefficients:

Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

(Intercept) 698.93 10.3644 67.436 9.487e-227 678.560 719.306 418

str -2.28 0.5195 -4.389 1.447e-05 -3.301 -1.259 418

Multiple R-squared: 0.05124 , Adjusted R-squared: 0.04897

F-statistic: 19.26 on 1 and 418 DF, p-value: 1.447e-05Fixing Heteroskedasticity III

| term | estimate | std.error | statistic | p.value | conf.low | conf.high | df | outcome |

|---|---|---|---|---|---|---|---|---|

| (Intercept) | 698.932952 | 10.3643599 | 67.436191 | 0.00e+00 | 678.560192 | 719.305713 | 418 | testscr |

| str | -2.279808 | 0.5194892 | -4.388557 | 1.45e-05 | -3.300945 | -1.258671 | 418 | testscr |

Showing The Effect of Heteroskedasticity (on se(ˆβ1))

modelsummary(models = list("Normal SE" = school_reg,

"Robust SE" = school_reg_robust),

fmt = 2, # round to 2 decimals

output = "html",

coef_rename = c("(Intercept)" = "Constant",

"str" = "STR"),

gof_map = list(

list("raw" = "nobs", "clean" = "n", "fmt" = 0),

list("raw" = "r.squared", "clean" = "R<sup>2</sup>", "fmt" = 2),

#list("raw" = "adj.r.squared", "clean" = "Adj. R<sup>2</sup>", "fmt" = 2),

list("raw" = "rmse", "clean" = "SER", "fmt" = 2)

),

escape = FALSE,

stars = c('*' = .1, '**' = .05, '***' = 0.01)

)| Normal SE | Robust SE | |

|---|---|---|

| Constant | 698.93*** | 698.93*** |

| (9.47) | (10.36) | |

| STR | −2.28*** | −2.28*** |

| (0.48) | (0.52) | |

| n | 420 | 420 |

| R2 | 0.05 | 0.05 |

| SER | 18.54 | 18.54 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

- What changed?

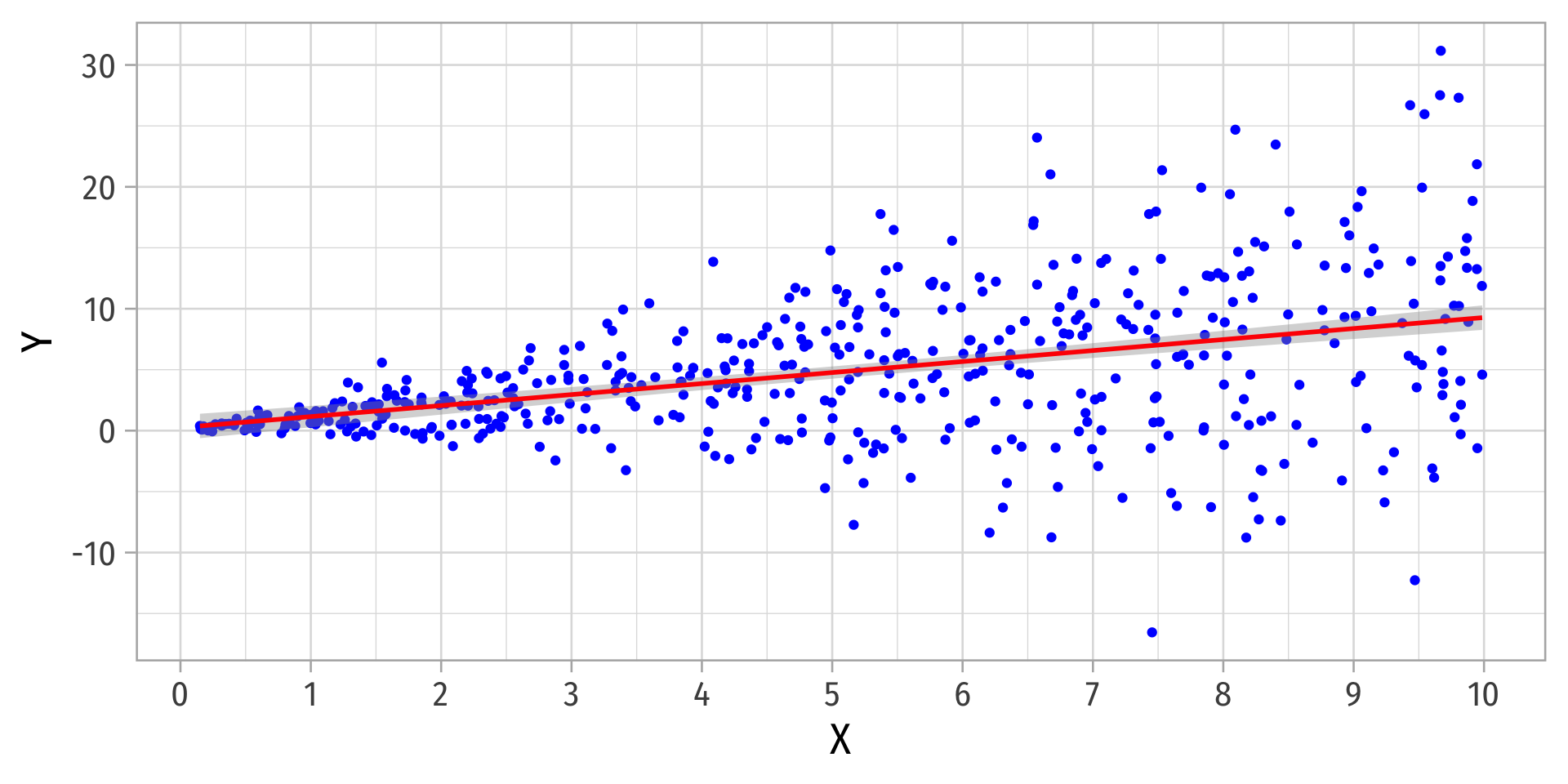

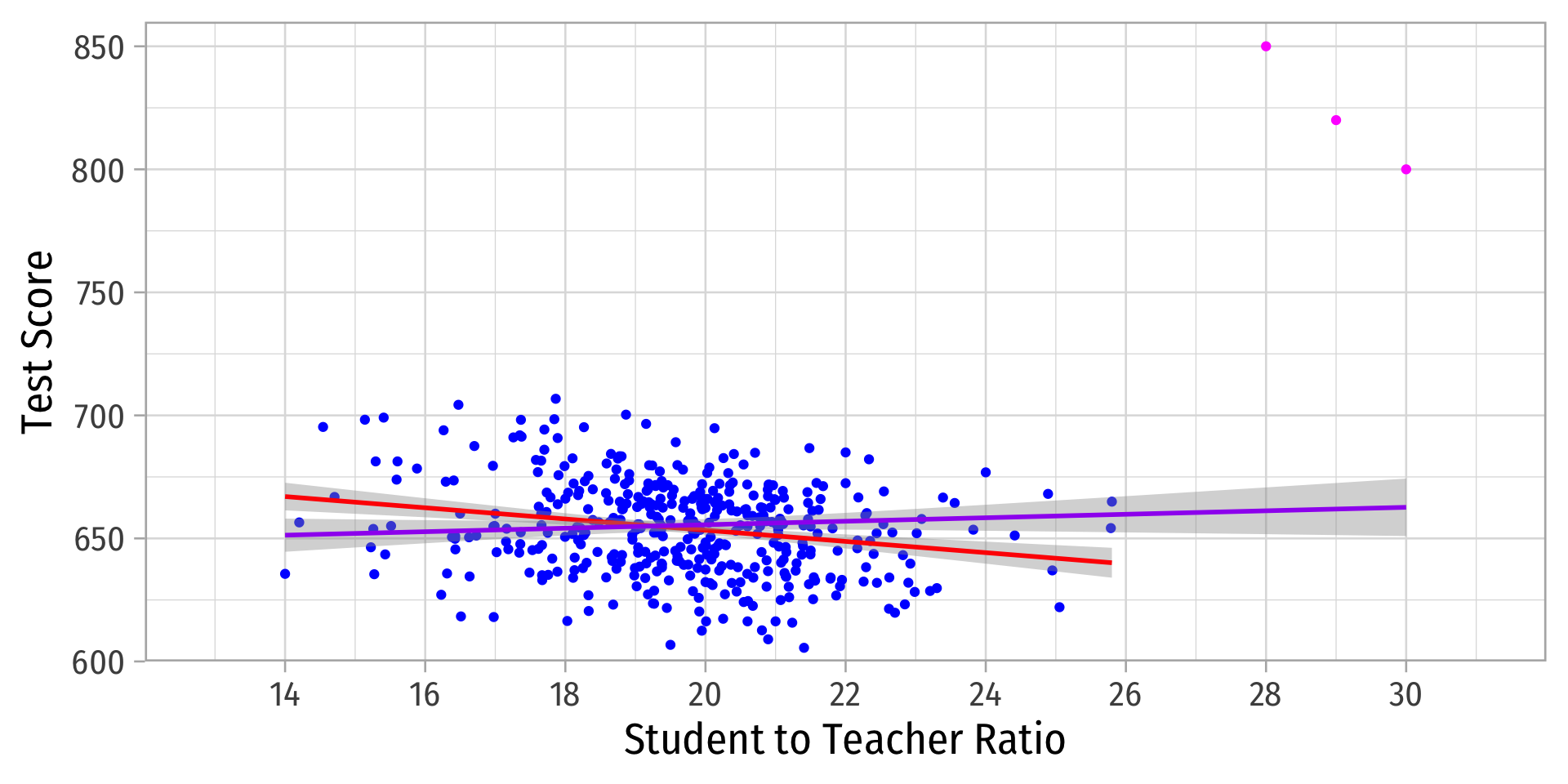

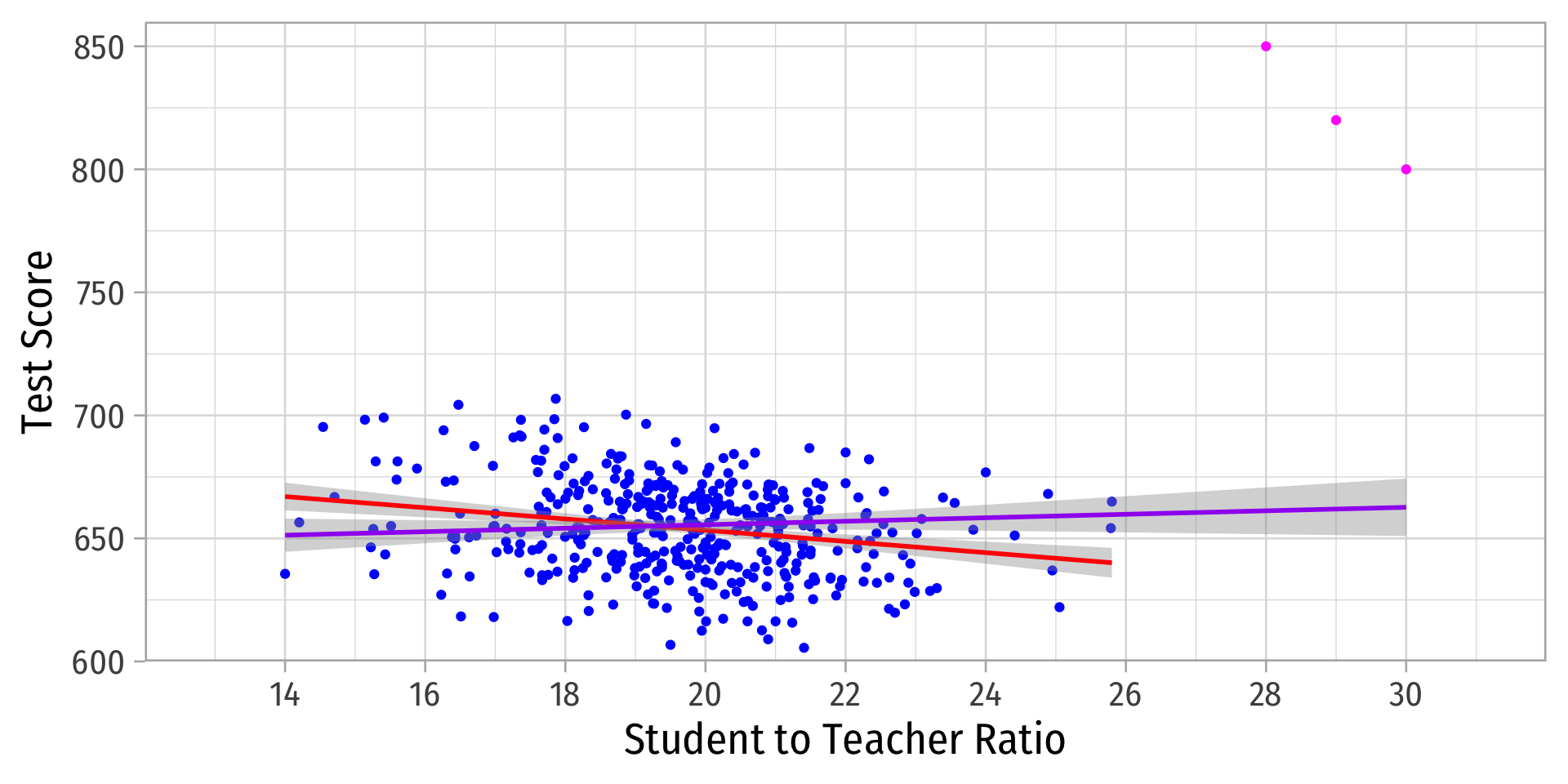

Outliers

Outliers Can Bias OLS! I

- Outliers can affect the slope (and intercept) of the line and add bias

- May be result of human error (measurement, transcribing, etc)

- May be meaningful and accurate

- In any case, compare how including/dropping outliers affects regression and always discuss outliers!

Outliers Can Bias OLS! II

Outliers Can Bias OLS! II

Outliers Can Bias OLS! III

| Original | With Outliers | |

|---|---|---|

| Constant | 698.93*** | 641.40*** |

| (9.47) | (11.21) | |

| STR | −2.28*** | 0.71 |

| (0.48) | (0.57) | |

| n | 420 | 423 |

| R2 | 0.05 | 0.00 |

| SER | 18.54 | 23.71 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

Detecting Outliers

- The

carpackage has anoutlierTestcommand to run on the regression

# install.packages("car")

library("car")

# Use Bonferonni test

outlierTest(school_outlier_reg) # will point out which obs #s seem outliers rstudent unadjusted p-value Bonferroni p

422 8.822768 3.0261e-17 1.2800e-14

423 7.233470 2.2493e-12 9.5147e-10

421 6.232045 1.1209e-09 4.7414e-07# find these observations

ca_school_outliers %>%

slice(c(422,423,421)) # find observations 422, 423, 421| observat | district | testscr | str |

|---|---|---|---|

| 422 | Crazy District 2 | 850 | 28 |

| 423 | Crazy District 3 | 820 | 29 |

| 421 | Crazy District 1 | 800 | 30 |