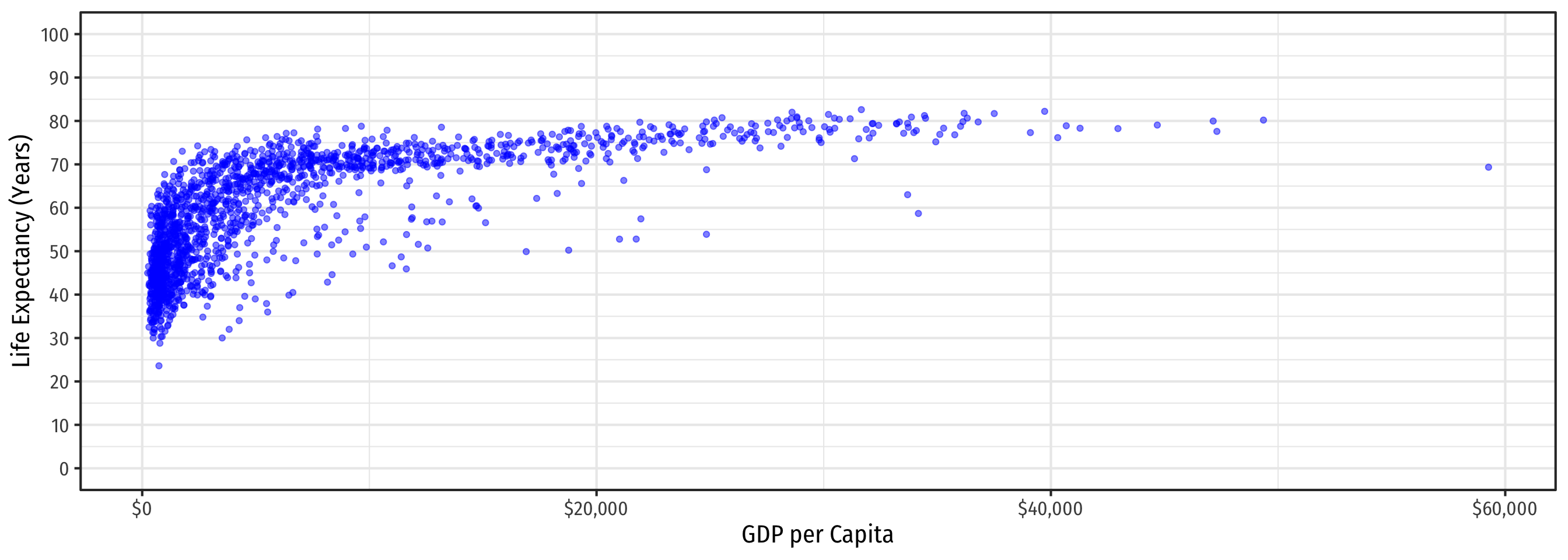

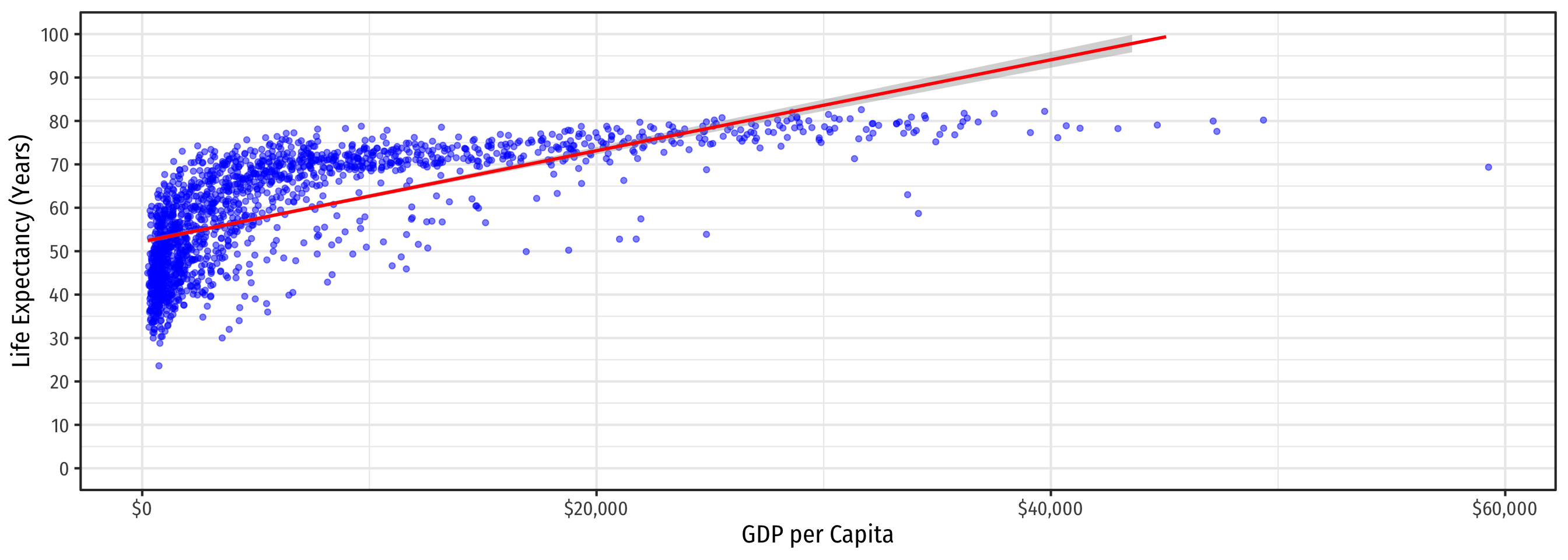

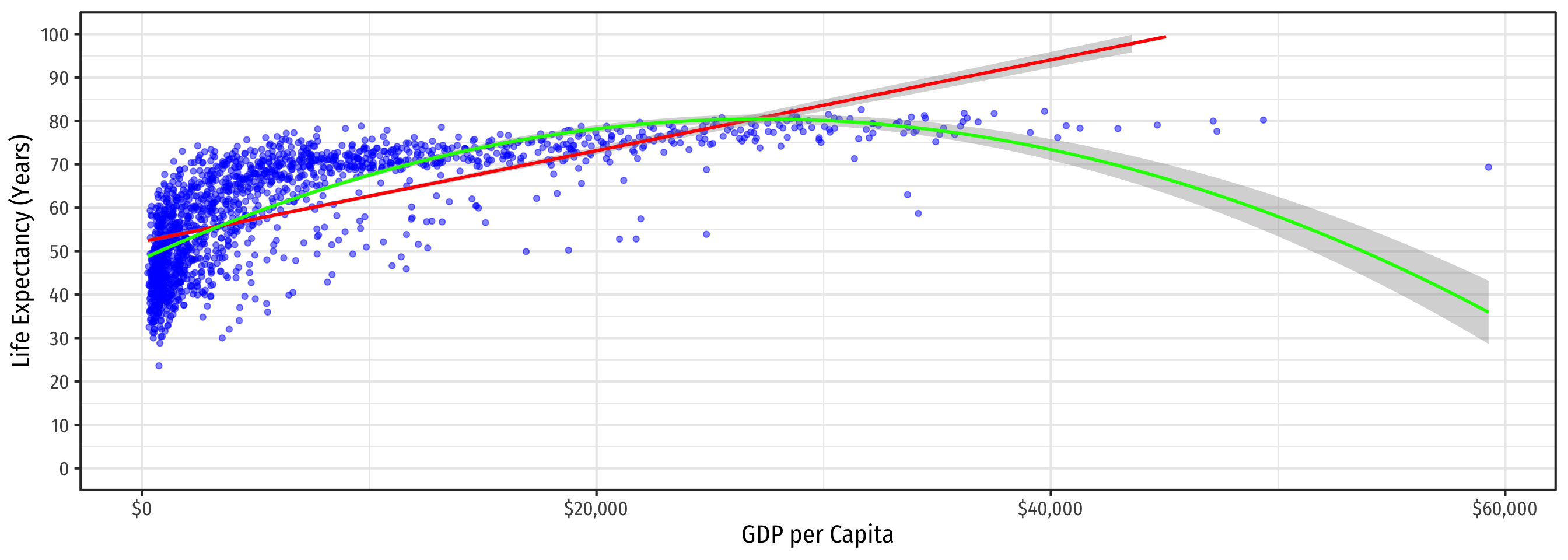

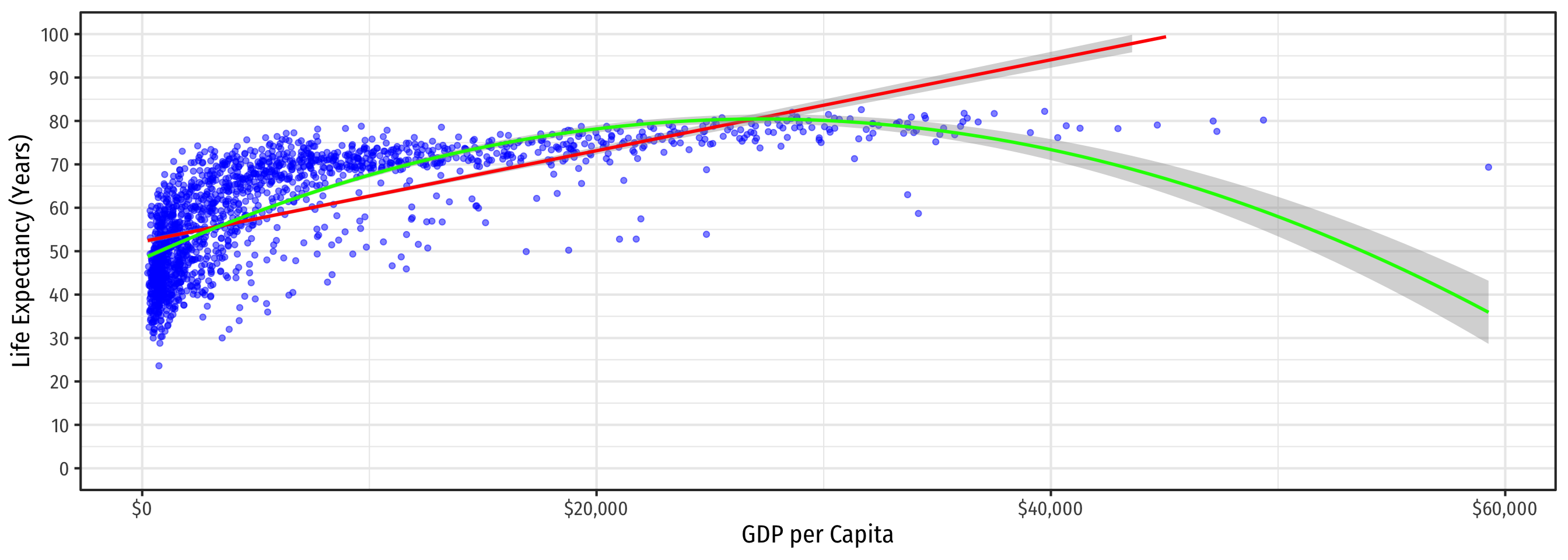

Linear Regression

Linear Regression

\[\color{red}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP}_i}\]

Linear Regression

\[\color{red}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP}_i}\]

\[\color{green}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP}_i+\hat{\beta_2}\text{GDP}_i^2}\]

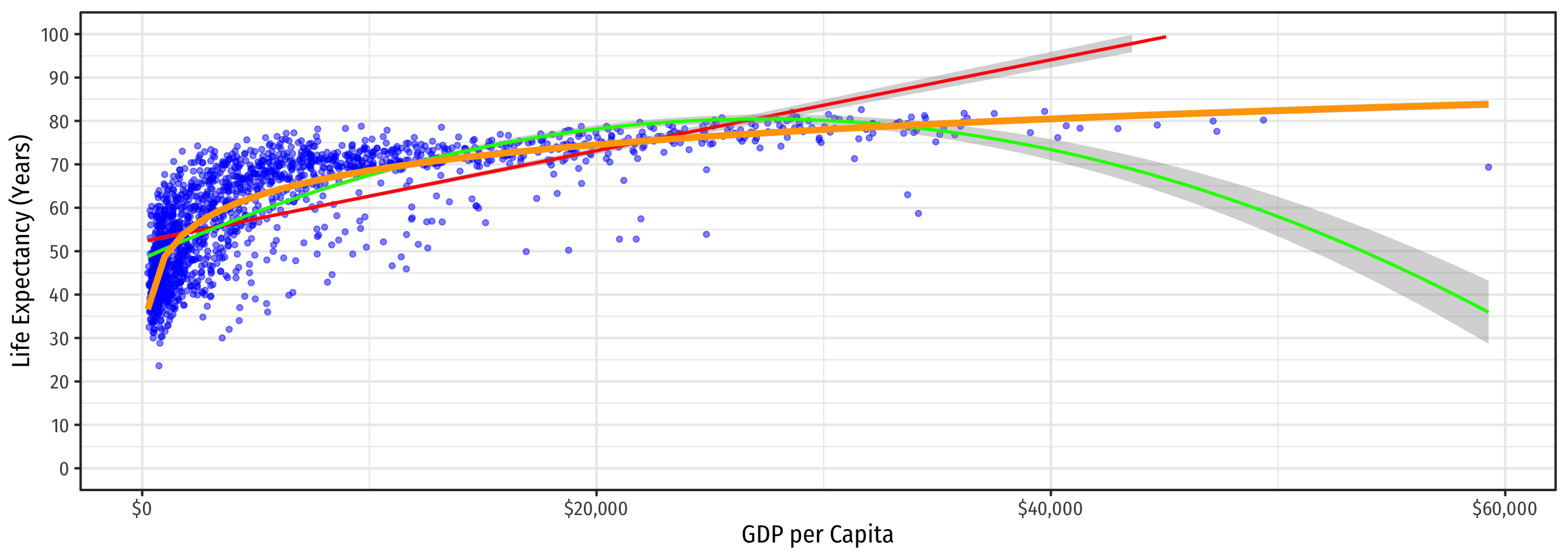

Linear Regression

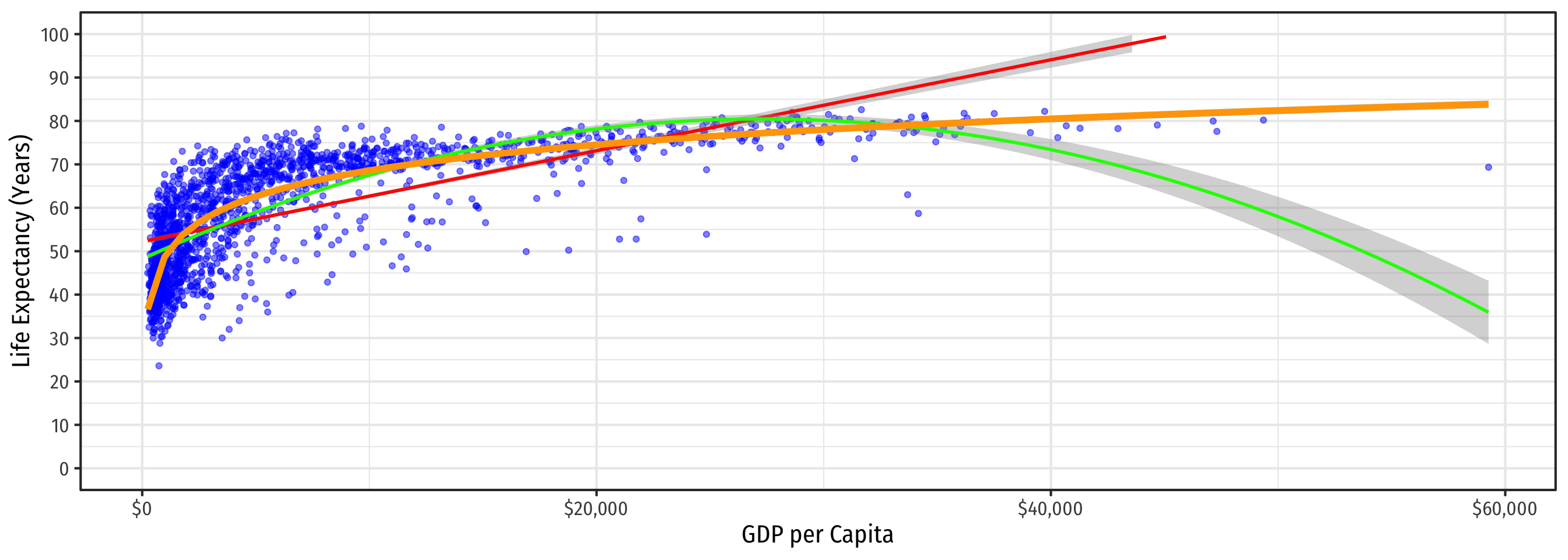

\[\color{red}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP}_i}\]

\[\color{green}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP}_i+\hat{\beta_2}\text{GDP}_i^2}\]

\[\color{orange}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\ln \text{GDP}_i}\]

Nonlinearities Alter Marginal Effects

- Polynomial:

\[Y=\hat{\beta_0}+\hat{\beta_1}X+\hat{\beta_2}X^2\]

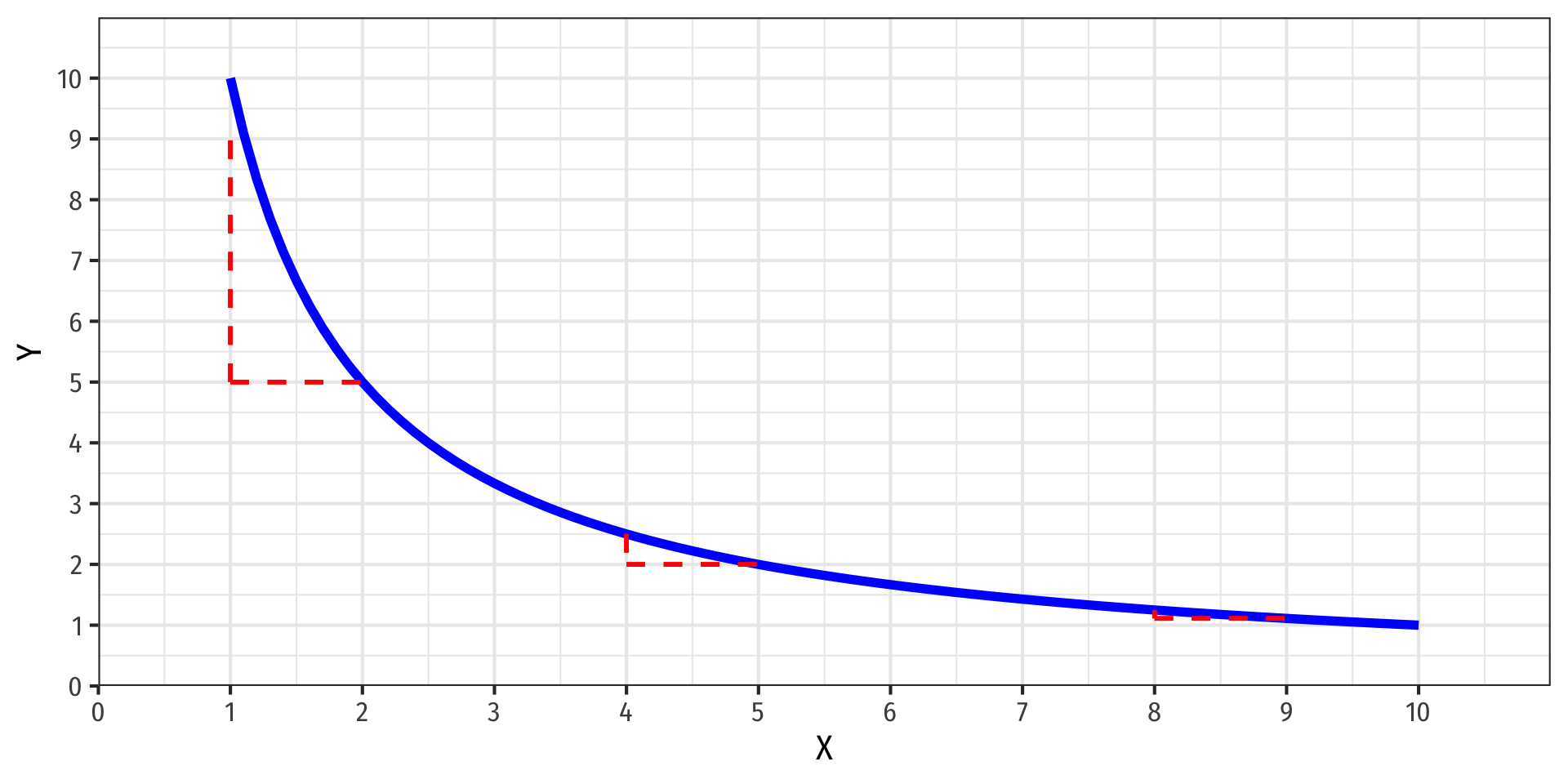

- Marginal effect, “slope” \(\left(\neq \hat{\beta_1}\right)\) depends on the value of \(X\)!

Nonlinearities Alter Marginal Effects

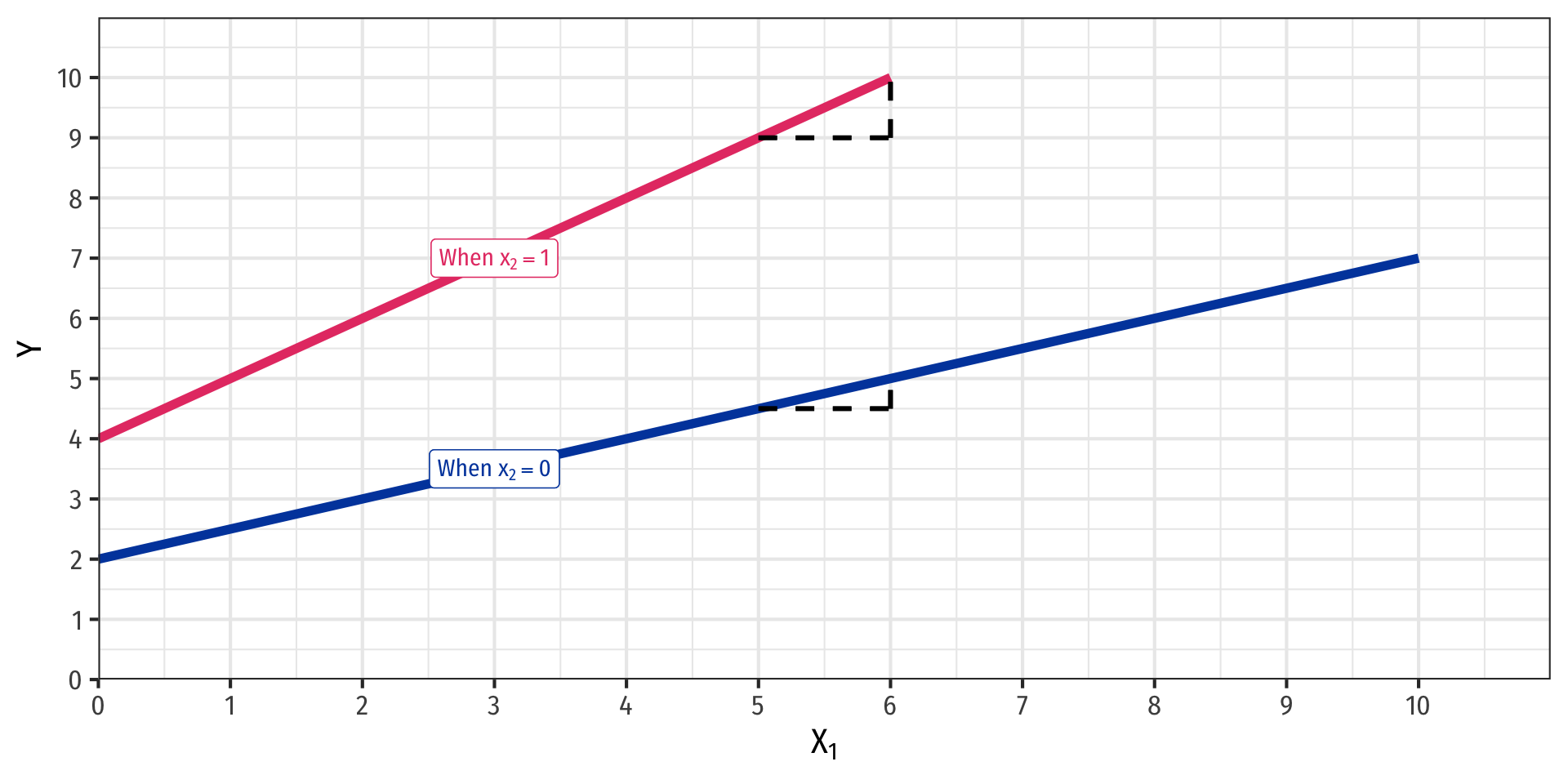

- Interaction Effect:

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X_1+\hat{\beta_2}X_2+\hat{\beta_3}X_1 \times X_2\]

Marginal effect, “slope” depends on the value of \(X_2\)!

Easy example: if \(X_2\) is a dummy variable:

- \(X_2=0\) (control) vs. \(X_2=1\) (treatment)

Polynomial Functions of \(X\) I

- Linear

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X\]

Polynomial Functions of \(X\) I

- Linear

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X\]

- Quadratic

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X+\hat{\beta_2}X^2\]

Polynomial Functions of \(X\) I

- Linear

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X\]

- Quadratic

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X+\hat{\beta_2}X^2\]

- Cubic

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X+\hat{\beta_2}X^2+\hat{\beta_3}X^3\]

Polynomial Functions of \(X\) I

- Linear

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X\]

- Quadratic

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X+\hat{\beta_2}X^2\]

- Cubic

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X+\hat{\beta_2}X^2+\hat{\beta_3}X^3\]

- Quartic

\[\hat{Y}=\hat{\beta_0}+\hat{\beta_1}X+\hat{\beta_2}X^2+\hat{\beta_3}X^3+\hat{\beta_4}X^4\]

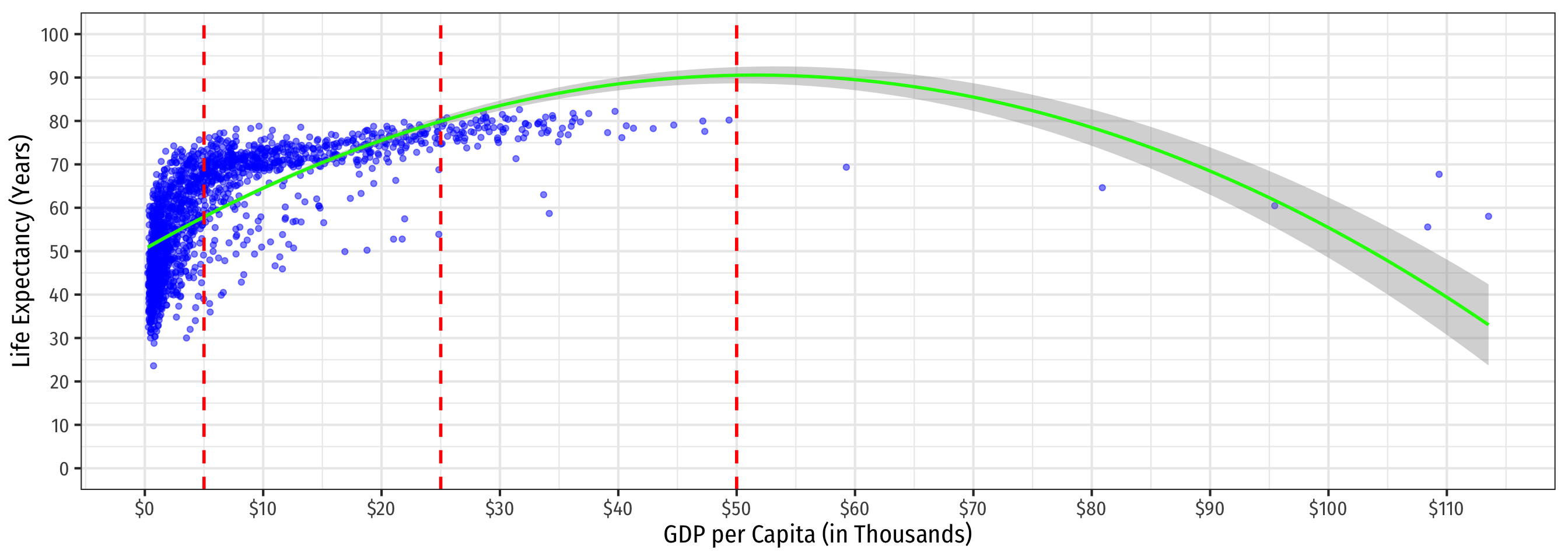

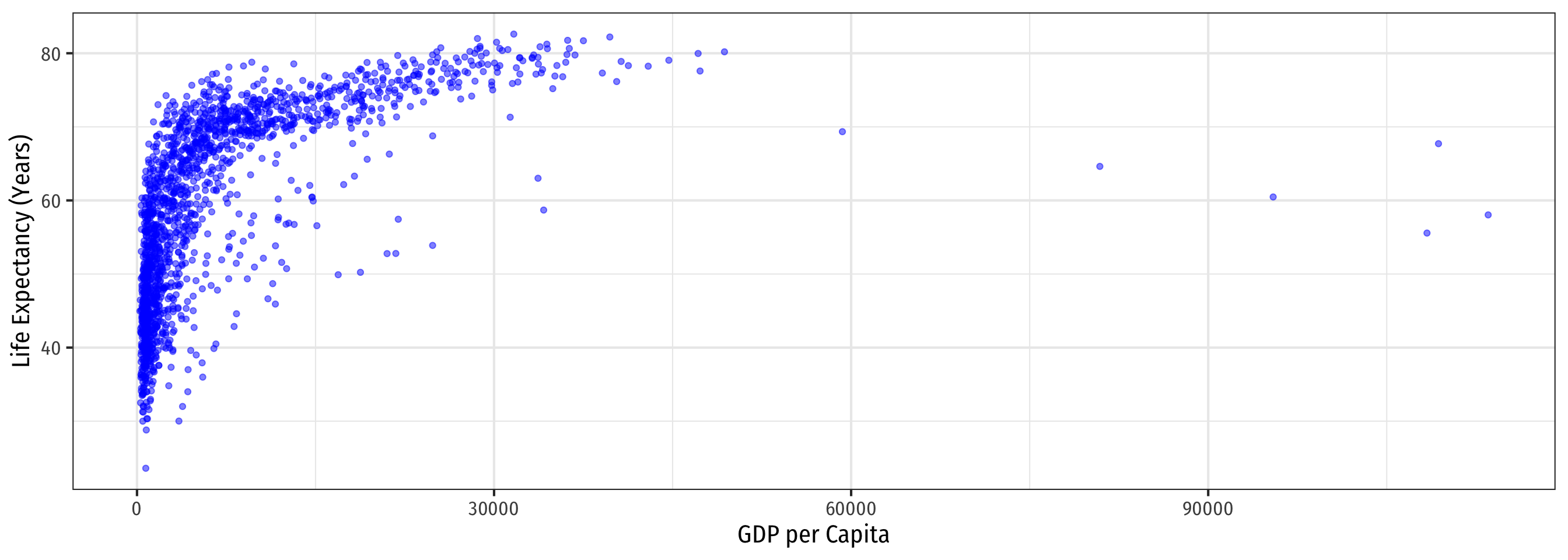

Quadratic Model: Example XII

Code

ggplot(data = gapminder)+

aes(x = GDP_t,

y = lifeExp)+

geom_point(color = "blue", alpha=0.5)+

stat_smooth(method = "lm",

formula = y ~ x + I(x^2),

color = "green")+

geom_vline(xintercept = c(5,25,50),

linetype = "dashed",

color = "red", size = 1)+

scale_x_continuous(labels = scales::dollar,

breaks = seq(0,120,10))+

scale_y_continuous(breaks = seq(0,100,10),

limits = c(0,100))+

labs(x = "GDP per Capita (in Thousands)",

y = "Life Expectancy (Years)")+

theme_bw(base_family = "Fira Sans Condensed",

base_size=16)

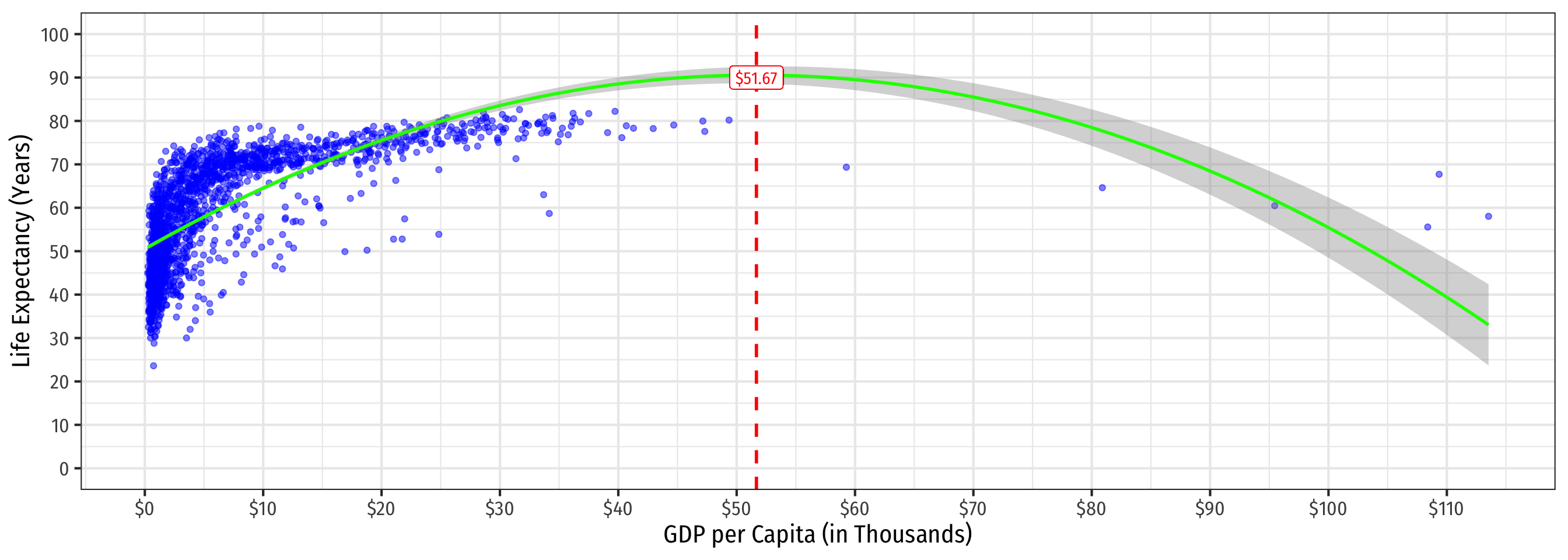

Quadratic Model: Maxima and Minima III

Code

ggplot(data = gapminder)+

aes(x = GDP_t,

y = lifeExp)+

geom_point(color = "blue", alpha=0.5)+

stat_smooth(method = "lm",

formula = y ~ x + I(x^2),

color = "green")+

geom_vline(xintercept=51.67, linetype="dashed", color="red", size = 1)+

geom_label(x=51.67, y=90, label="$51.67", color="red")+

scale_x_continuous(labels = scales::dollar,

breaks = seq(0,120,10))+

scale_y_continuous(breaks = seq(0,100,10),

limits = c(0,100))+

labs(x = "GDP per Capita (in Thousands)",

y = "Life Expectancy (Years)")+

theme_bw(base_family = "Fira Sans Condensed",

base_size=16)

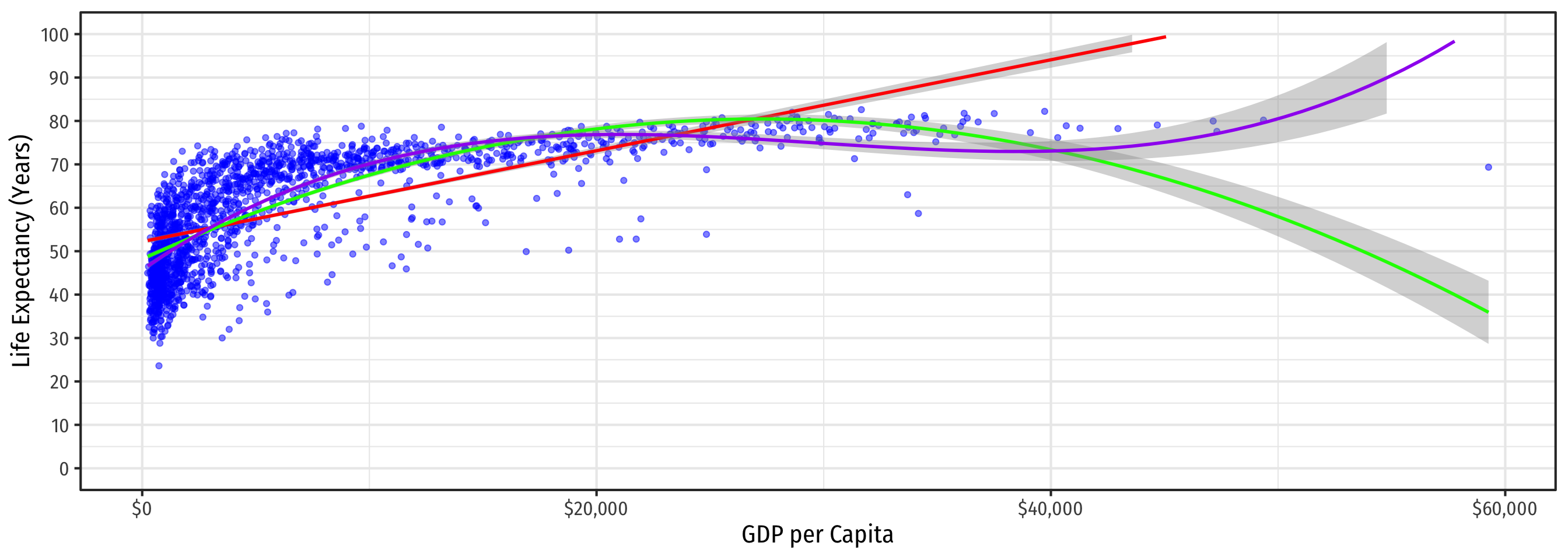

Determining Polynomials are Necessary II

- Should we keep going up in polynomials?

Determining Polynomials are Necessary II

- Should we keep going up in polynomials?

\[\color{#6A5ACD}{\widehat{\text{Life Expectancy}_i} = \hat{\beta_0}+\hat{\beta_1} GDP_i+\hat{\beta_2}GDP^2_i+\hat{\beta_3}GDP_i^3}\]

Determining Polynomials are Necessary III

In general, you should have a compelling theoretical reason why data or relationships should “change direction” multiple times

Or clear data patterns that have multiple “bends”

Recall, we care more about accurately measuring the causal effect of \(X \rightarrow Y\), rather than getting the most accurate prediction possible for \(\hat{Y}\)

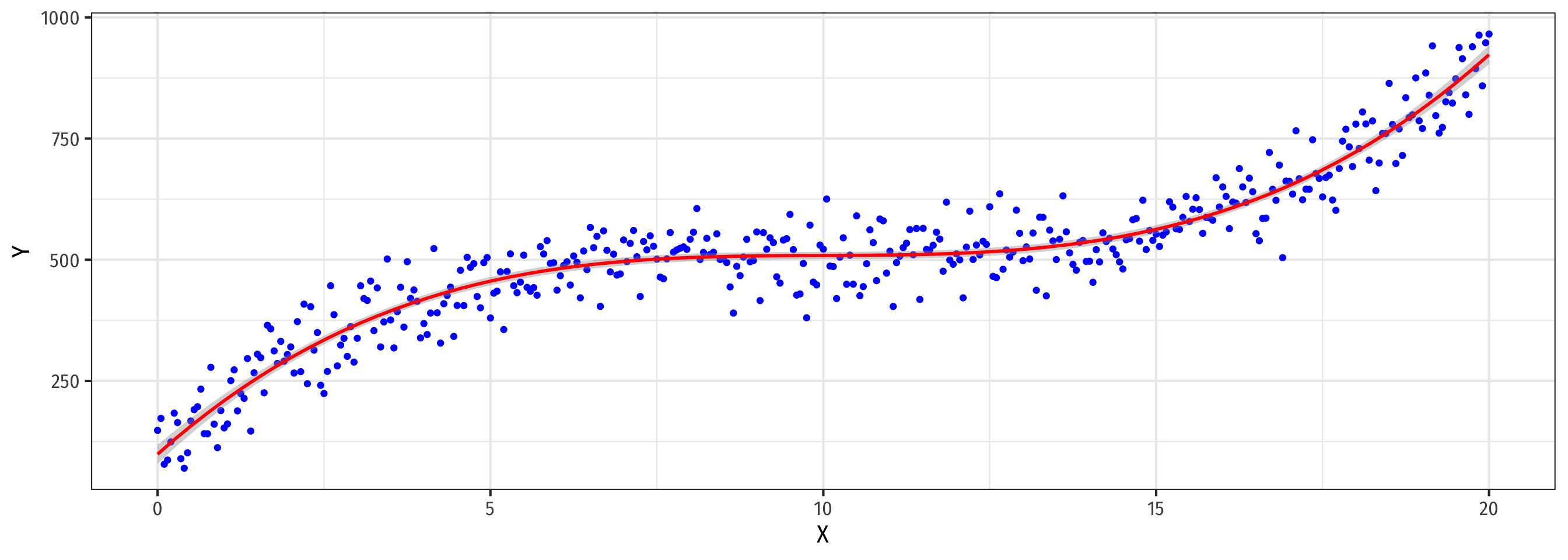

If You Kept Going…Visually

If You Kept Going…Visually

A 4th-degree polynomial

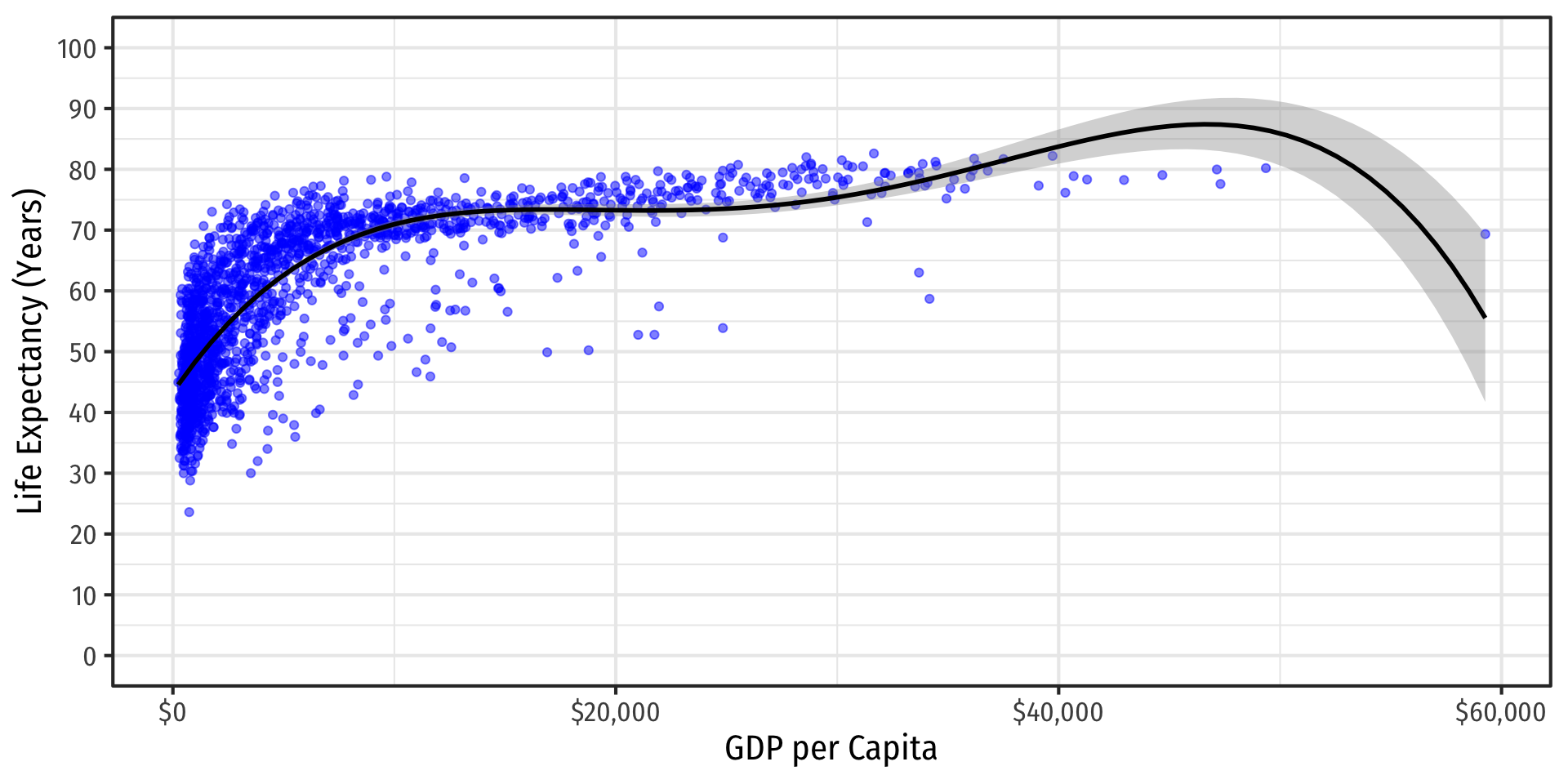

If You Kept Going…Visually

A 9th-degree polynomial

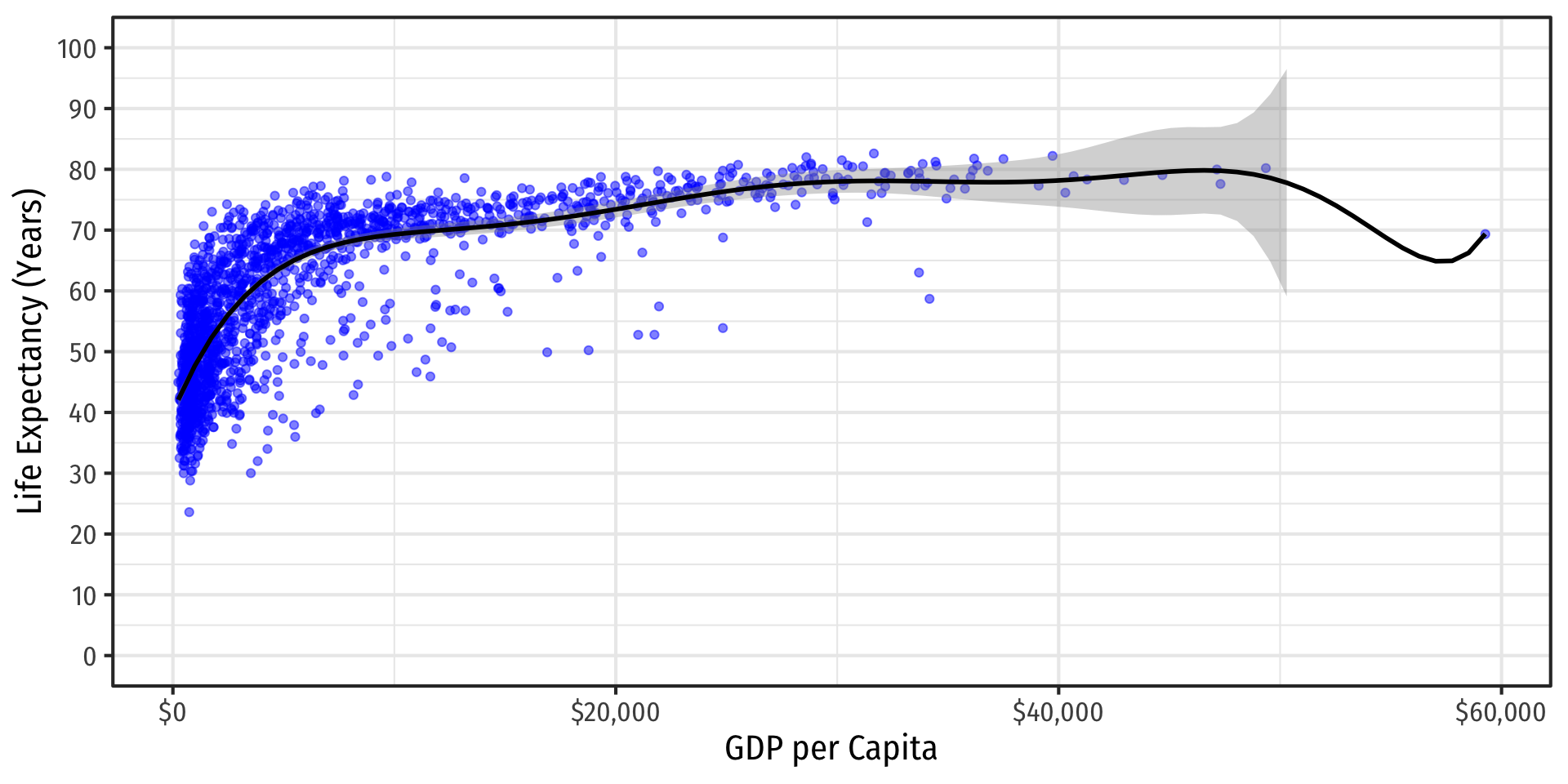

If You Kept Going…Visually

A 14th-degree polynomial

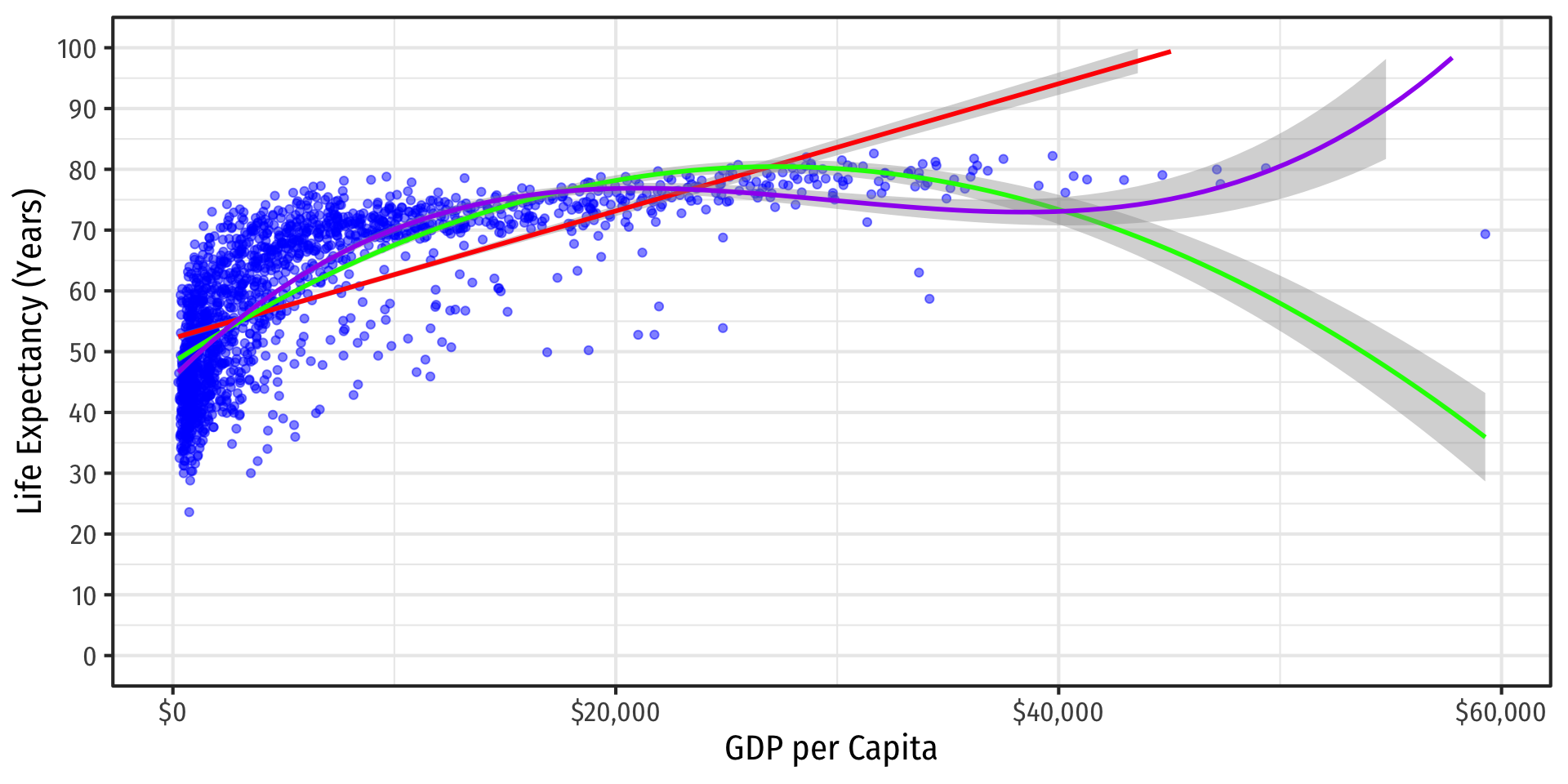

Linear Regression

\[\color{red}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP}_i}\]

\[\color{green}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP}_i+\hat{\beta_2}\text{GDP}_i^2}\]

\[\color{orange}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\ln \text{GDP}_i}\]

Logarithmic Models

- Another useful model for nonlinear data is the logarithmic model1

- We transform either \(X\), \(Y\), or both by taking the (natural) logarithm

- Logarithmic model has two additional advantages

- We can easily interpret coefficients as percentage changes or elasticities

- Useful economic shape: diminishing returns (production functions, utility functions, etc)

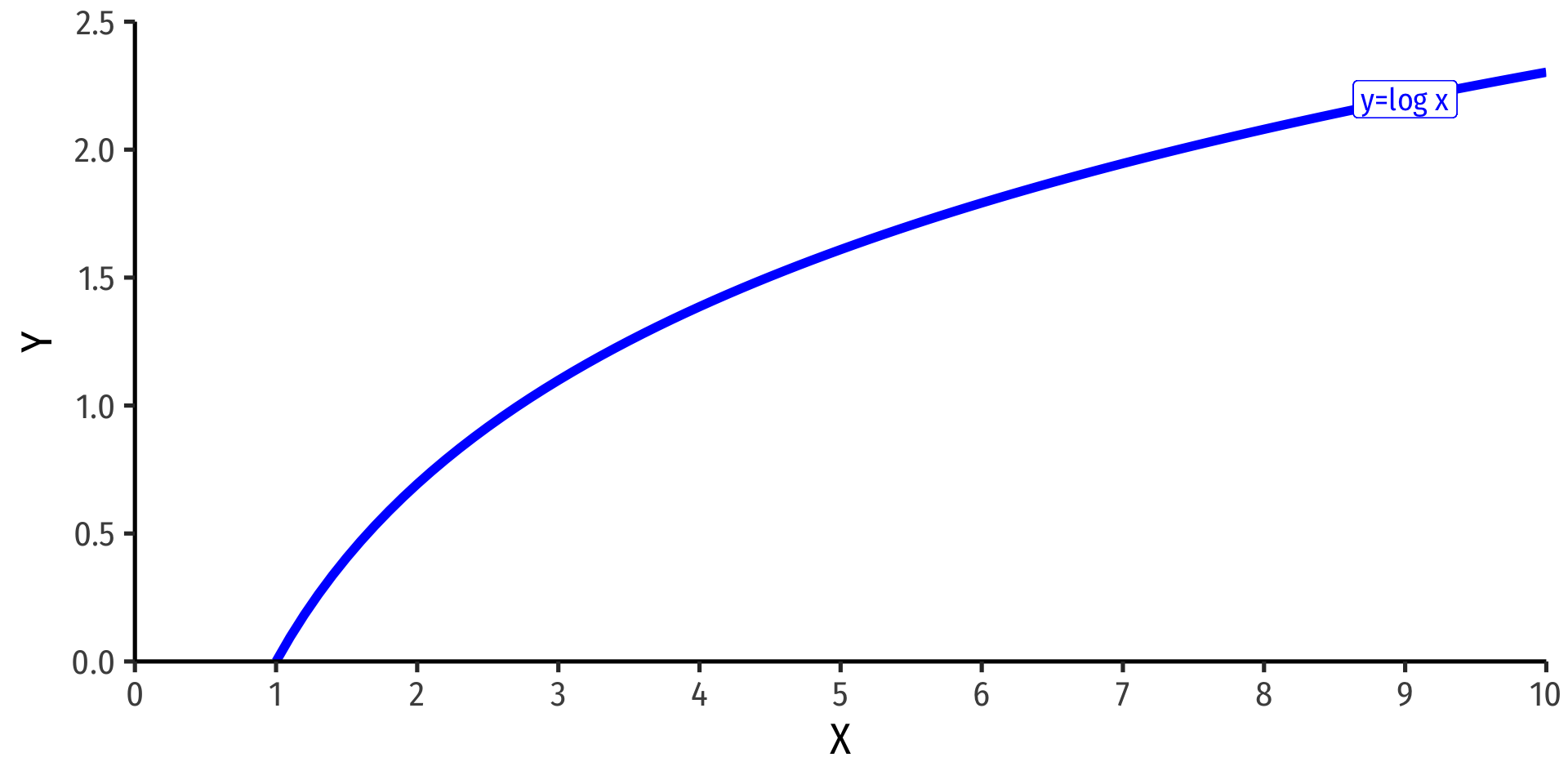

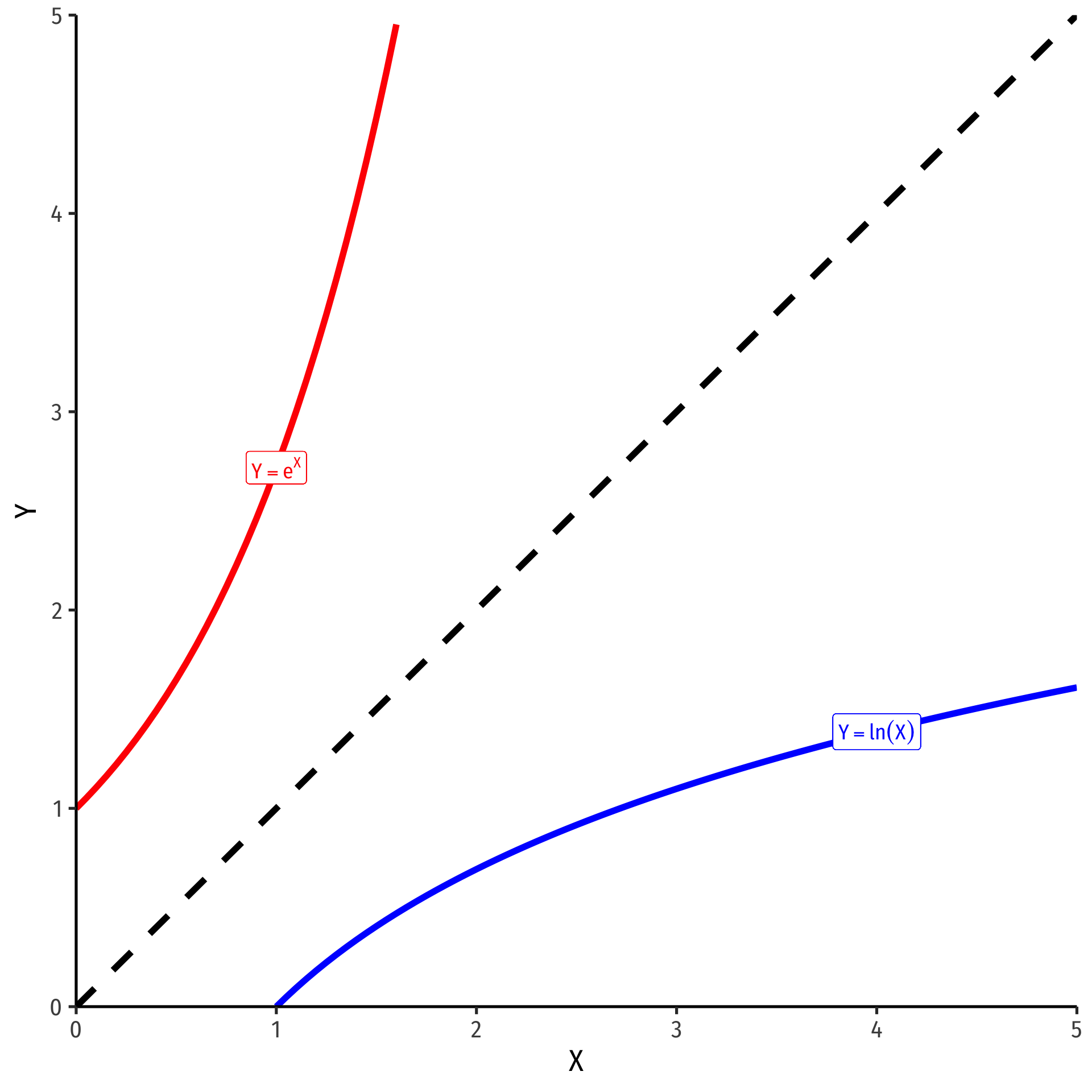

The Natural Logarithm

The exponential function, \(Y=e^X\) or \(Y=exp(X)\), where base \(e=2.71828...\)

Natural logarithm is the inverse, \(Y=ln(X)\)

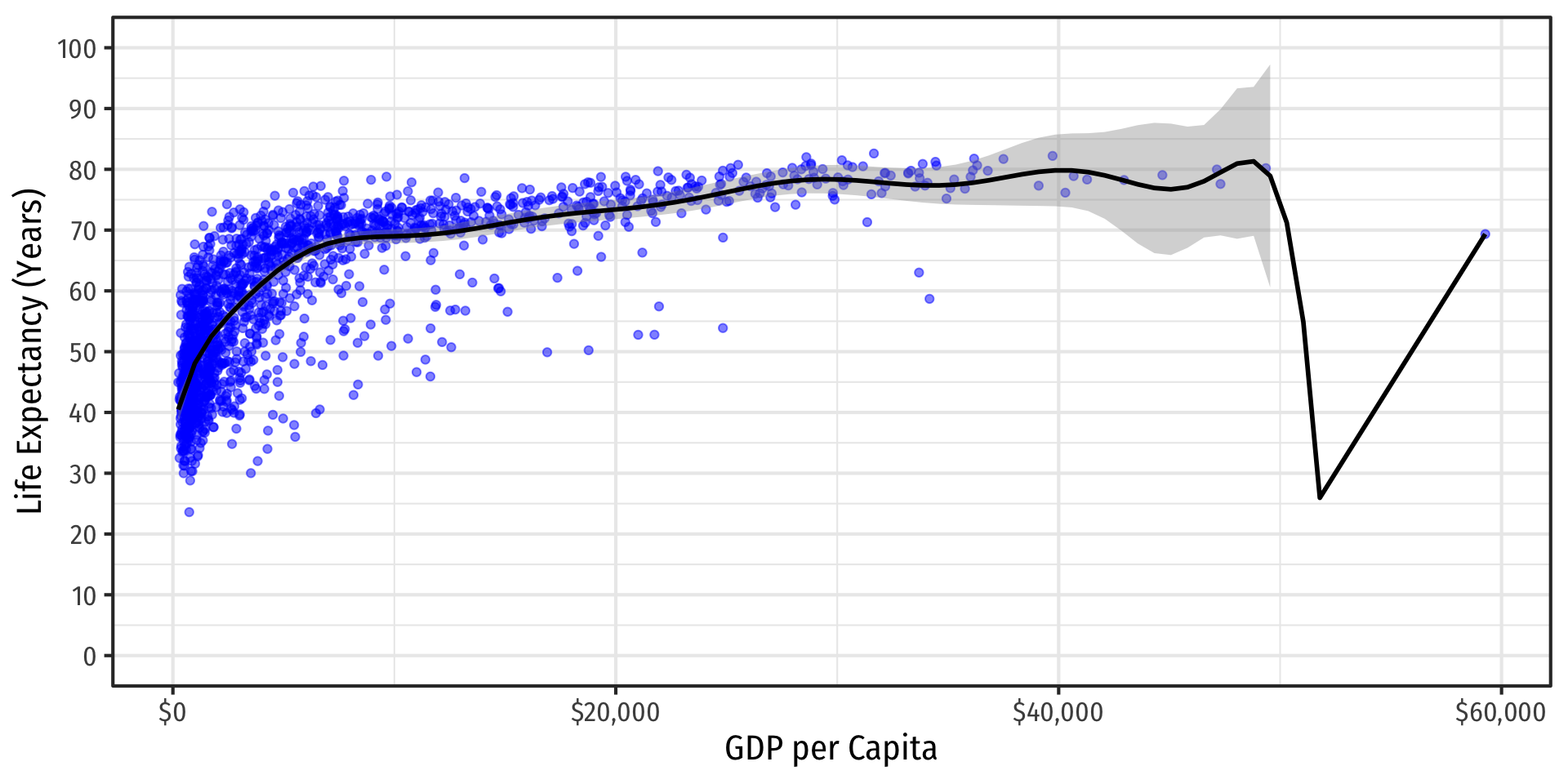

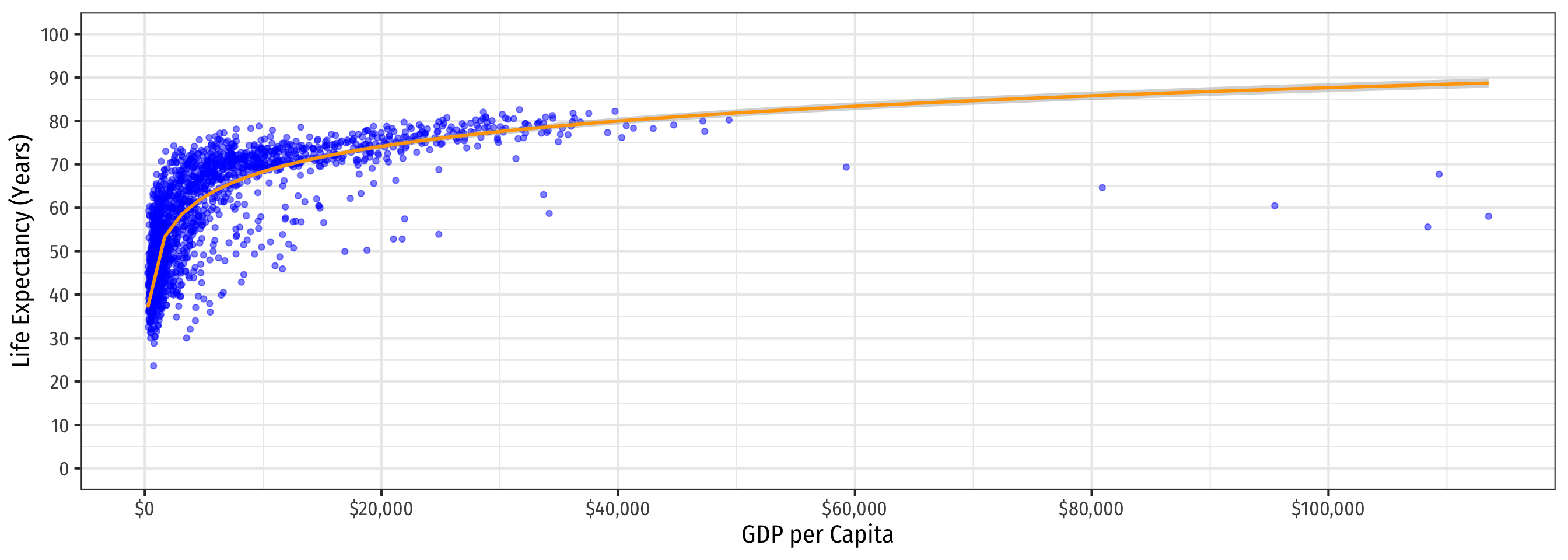

Linear-Log Model Graph (Linear X-Axis)

Code

ggplot(data = gapminder)+

aes(x = gdpPercap,

y = lifeExp)+

geom_point(color = "blue", alpha = 0.5)+

geom_smooth(method = "lm",

formula = y ~ log(x),

color = "orange")+

scale_x_continuous(labels = scales::dollar,

breaks = seq(0,120000,20000))+

scale_y_continuous(breaks = seq(0,100,10),

limits = c(0,100))+

labs(x = "GDP per Capita",

y = "Life Expectancy (Years)")+

theme_bw(base_family = "Fira Sans Condensed",

base_size = 16)

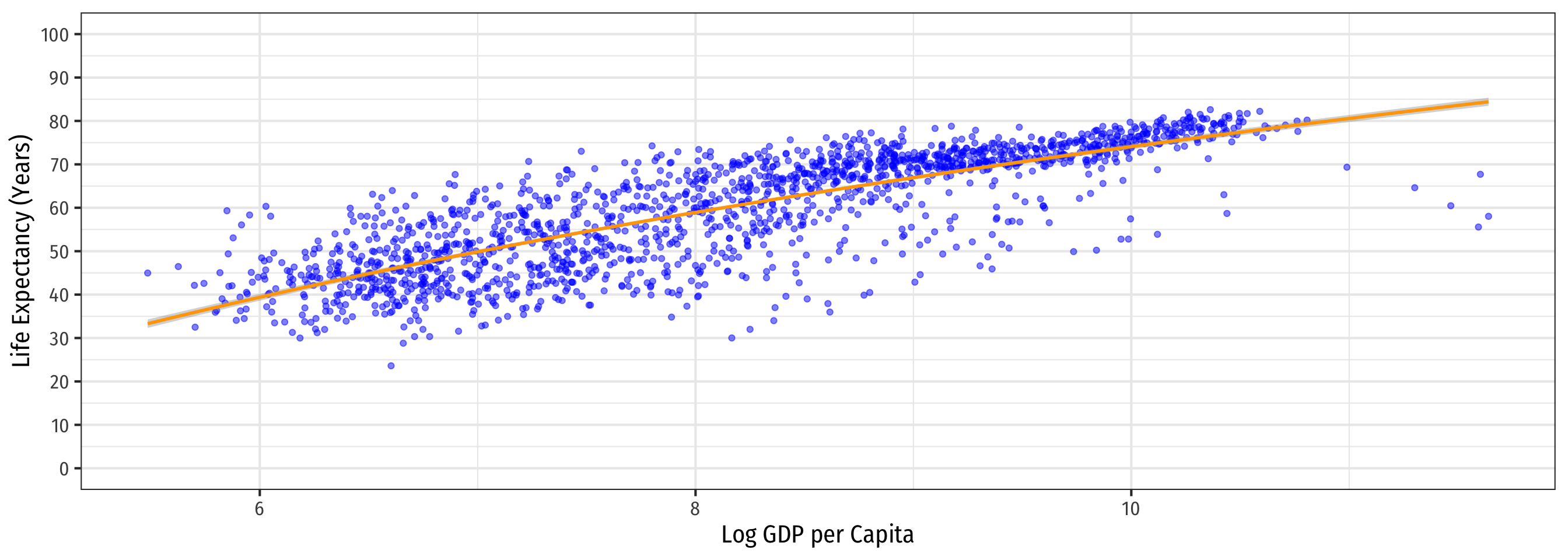

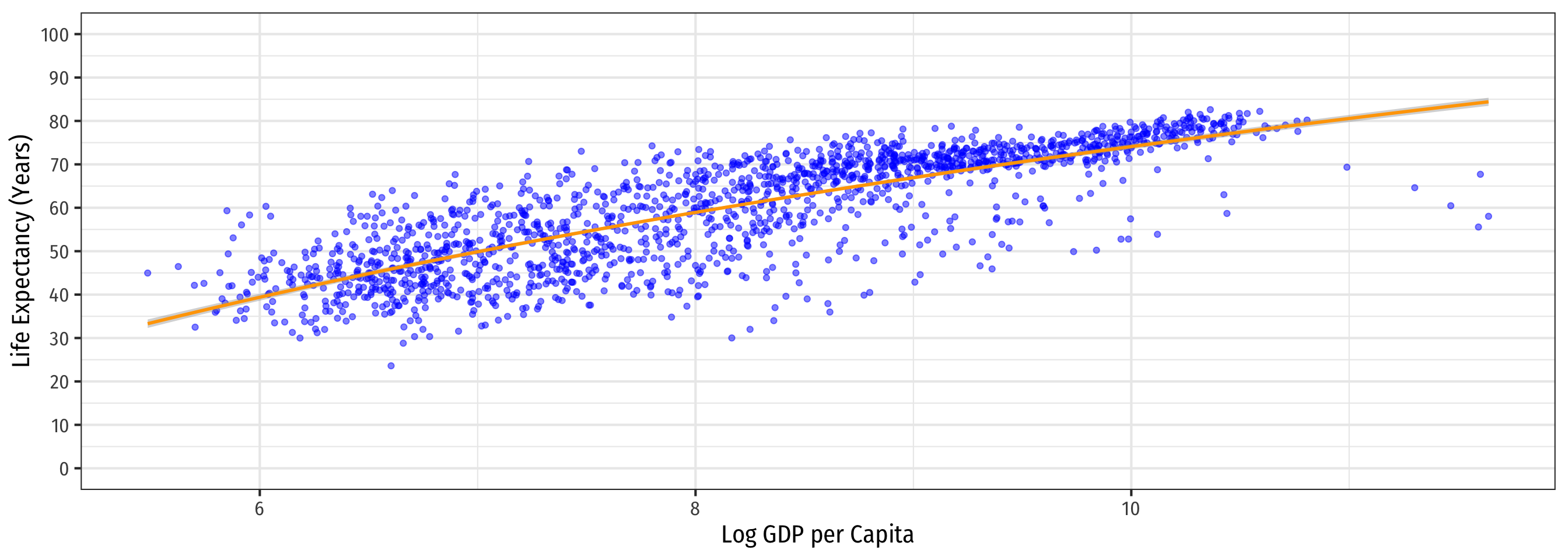

Linear-Log Model Graph (Log X-Axis)

Code

ggplot(data = gapminder)+

aes(x = loggdp,

y = lifeExp)+

geom_point(color = "blue", alpha = 0.5)+

geom_smooth(method = "lm",

formula = y ~ log(x),

color = "orange")+

scale_y_continuous(breaks = seq(0,100,10),

limits = c(0,100))+

labs(x = "Log GDP per Capita",

y = "Life Expectancy (Years)")+

theme_bw(base_family = "Fira Sans Condensed",

base_size = 16)

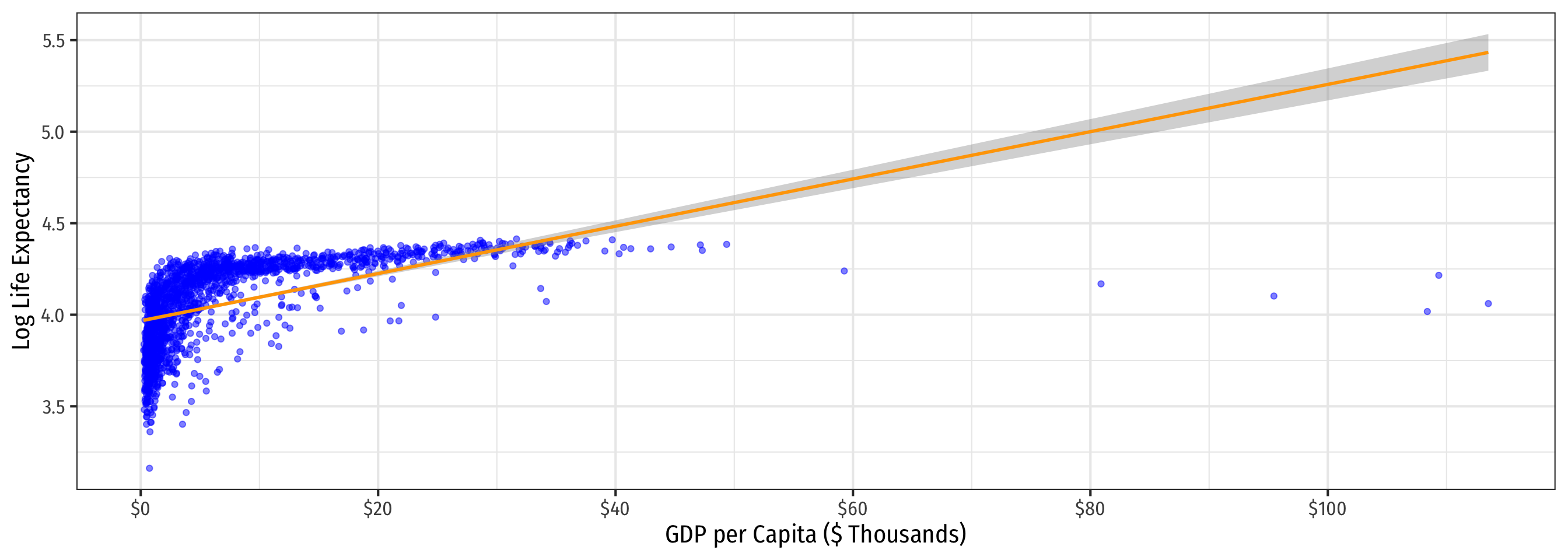

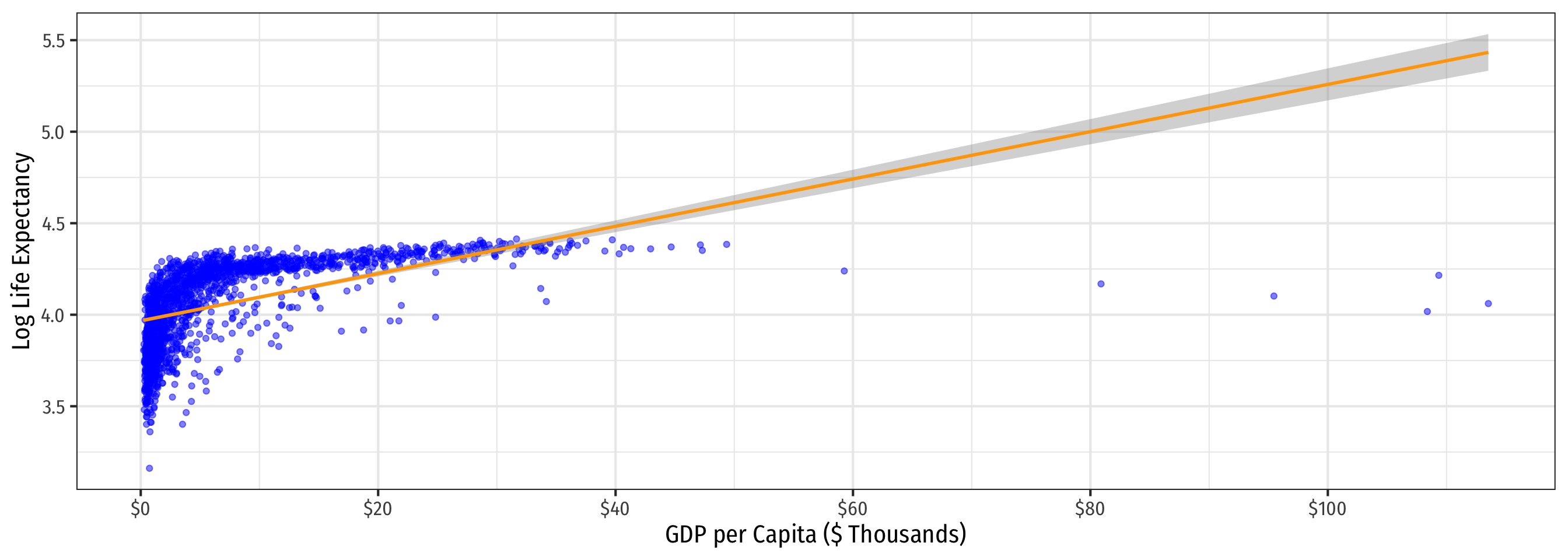

Linear-Log Model Graph

Code

ggplot(data = gapminder)+

aes(x = gdp_t,

y = loglife)+

geom_point(color = "blue", alpha = 0.5)+

geom_smooth(method = "lm", color = "orange")+

scale_x_continuous(labels = scales::dollar,

breaks = seq(0,120,20))+

labs(x = "GDP per Capita ($ Thousands)",

y = "Log Life Expectancy")+

theme_bw(base_family = "Fira Sans Condensed",

base_size = 16)

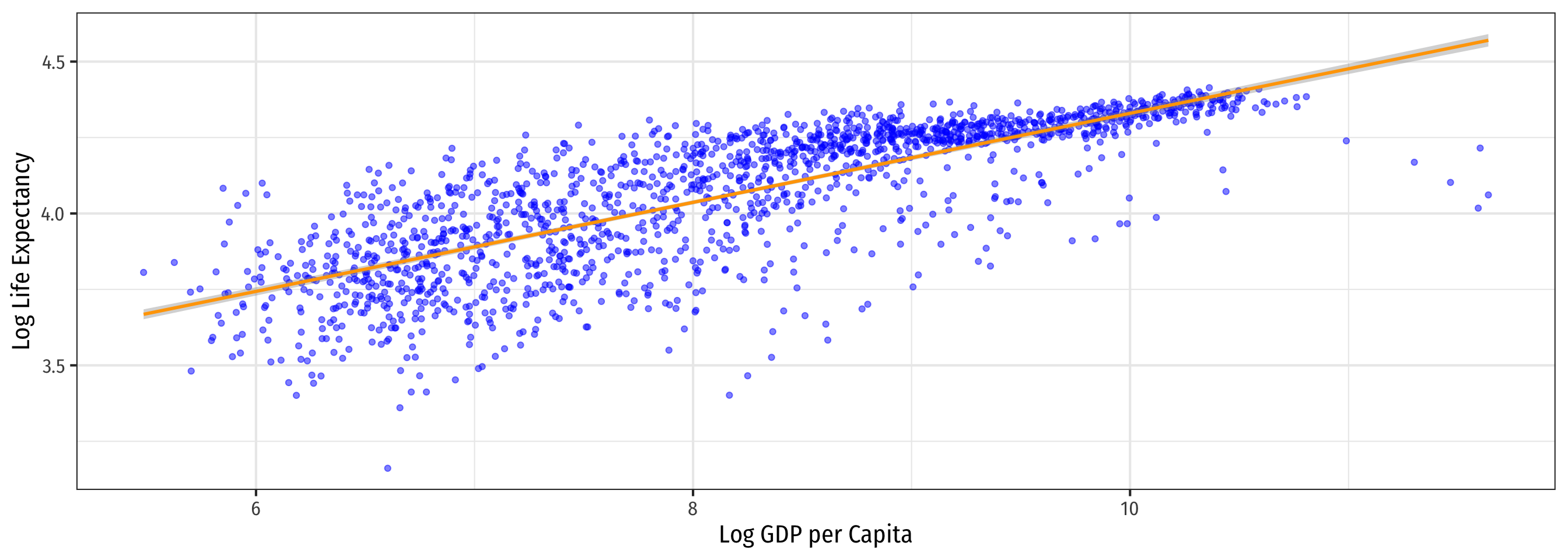

Log-Log Model Graph

Comparing Models III

| Linear-Log | Log-Linear | Log-Log |

|---|---|---|

|

|

|

| \(\hat{Y_i}=\hat{\beta_0}+\hat{\beta_1}\color{#e64173}{\ln X_i}\) | \(\color{#e64173}{\ln Y_i}=\hat{\beta_0}+\hat{\beta_1}X_i\) | \(\color{#e64173}{\ln Y_i}=\hat{\beta_0}+\hat{\beta_1}\color{#e64173}{\ln X_i}\) |

| \(R^2=0.65\) | \(R^2=0.30\) | \(R^2=0.61\) |

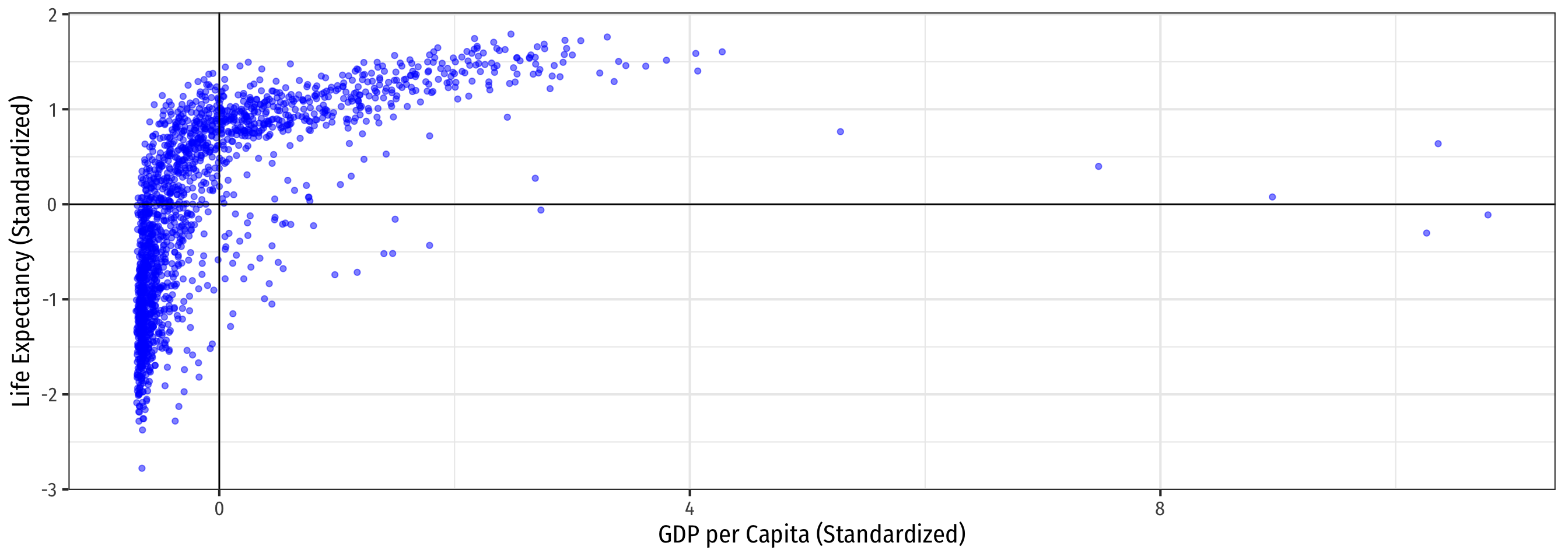

Rescaling: Visually

Rescaling: Visually

All F-test II

- Alternatively, if you use

broominstead ofsummary():glance()command makes table of regression summary statisticstidy()only shows coefficients

statisticis the All F-test,p.valuenext to it is the p-value from the F test