4.1 — Multivariate OLS Estimators

ECON 480 • Econometrics • Fall 2022

Dr. Ryan Safner

Associate Professor of Economics

safner@hood.edu

ryansafner/metricsF22

metricsF22.classes.ryansafner.com

Contents

The Multivariate OLS Estimators

The Expected Value of ˆβj: Bias

The Multivariate OLS Estimators

The Multivariate OLS Estimators

Yi=β0+β1X1i+β2X2i+⋯+βkXki+ui

- The ordinary least squares (OLS) estimators of the unknown population parameters β0,β1,β2,⋯,βk solves:

min^β0,^β1,^β2,⋯,^βkn∑i=1[Yi−(^β0+^β1X1i+^β2X2i+⋯+^βkXki)⏟ˆYi⏟ˆui]2

- Again, OLS estimators are chosen to minimize the sum of squared residuals (SSR)

- i.e. sum of squared “distances” between actual values of Yi and predicted values ^Yi

The Multivariate OLS Estimators: FYI

Math FYI

in linear algebra terms, a regression model with n observations of k independent variables:

Y=Xβ+u

(y1y2⋮yn)⏟Y(n×1)=(x1,1x1,2⋯x1,nx2,1x2,2⋯x2,n⋮⋮⋱⋮xk,1xk,2⋯xk,n)⏟X(n×k)(β1β2⋮βk)⏟β(k×1)+(u1u2⋮un)⏟u(n×1)

The OLS estimator for β is ˆβ=(X′X)−1X′Y 😱

Appreciate that I am saving you from such sorrow 🤖

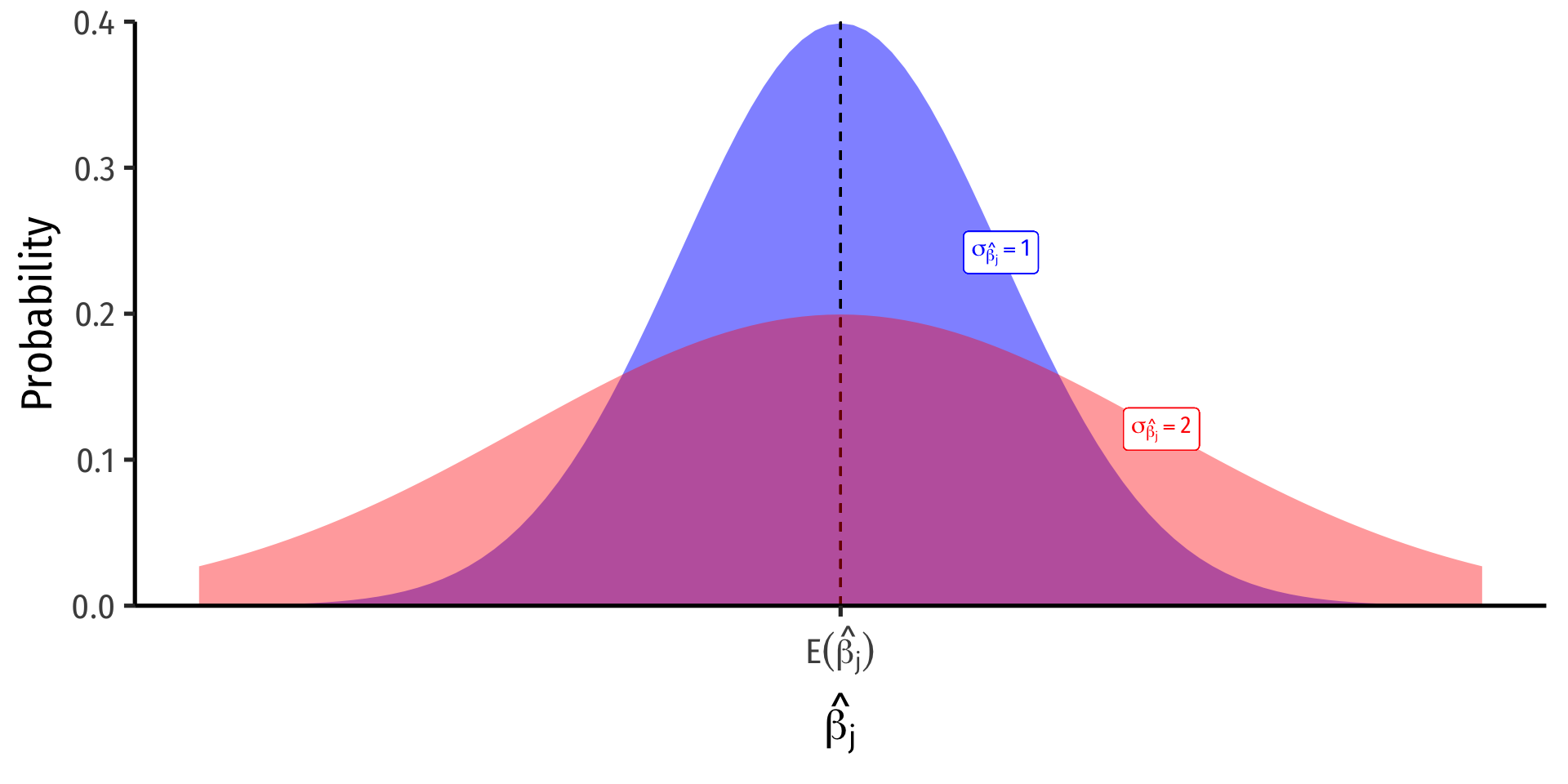

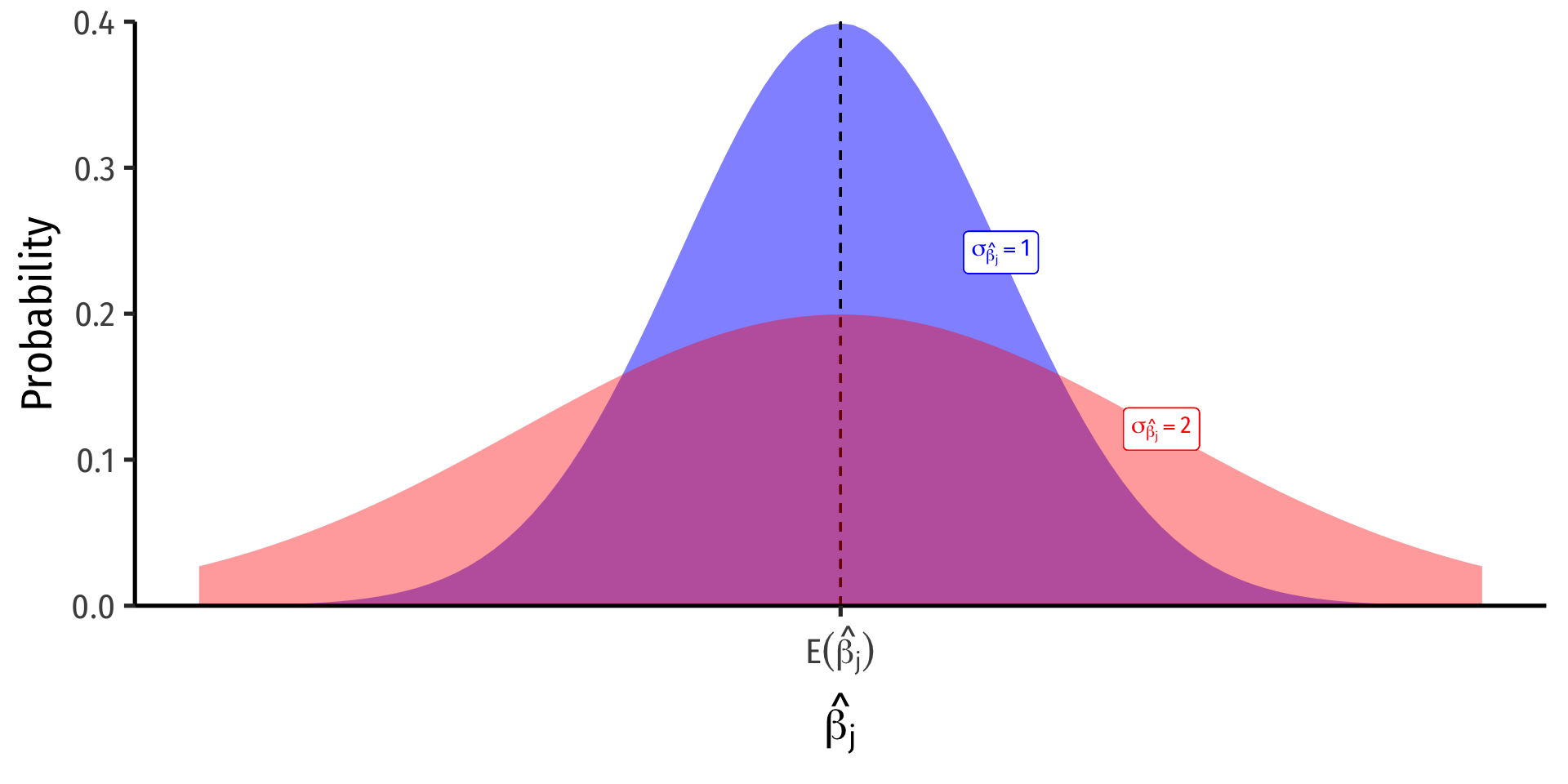

The Sampling Distribution of ^βj

- For any individual βj, it has a sampling distribution:

^βj∼N(E[^βj],se(^βj))

- We want to know its sampling distribution’s:

- Center: E[^βj]; what is the expected value of our estimator?

- Spread: se(^βj); how precise or uncertain is our estimator?

The Sampling Distribution of ^βj

- For any individual βj, it has a sampling distribution:

^βj∼N(E[^βj],se(^βj))

- We want to know its sampling distribution’s:

- Center: E[^βj]; what is the expected value of our estimator?

- Spread: se(^βj); how precise or uncertain is our estimator?

The Expected Value of ^βj: Bias

Exogeneity and Unbiasedness

- As before, E[^βj]=βj when Xj is exogenous (i.e. cor(Xj,u)=0)

- We know the true E[^βj]=βj+cor(Xj,u)σuσXj⏟O.V. Bias

- If Xj is endogenous (i.e. cor(Xj,u)≠0), contains omitted variable bias

- Let’s “see” an example of omitted variable bias and quantify it with our example

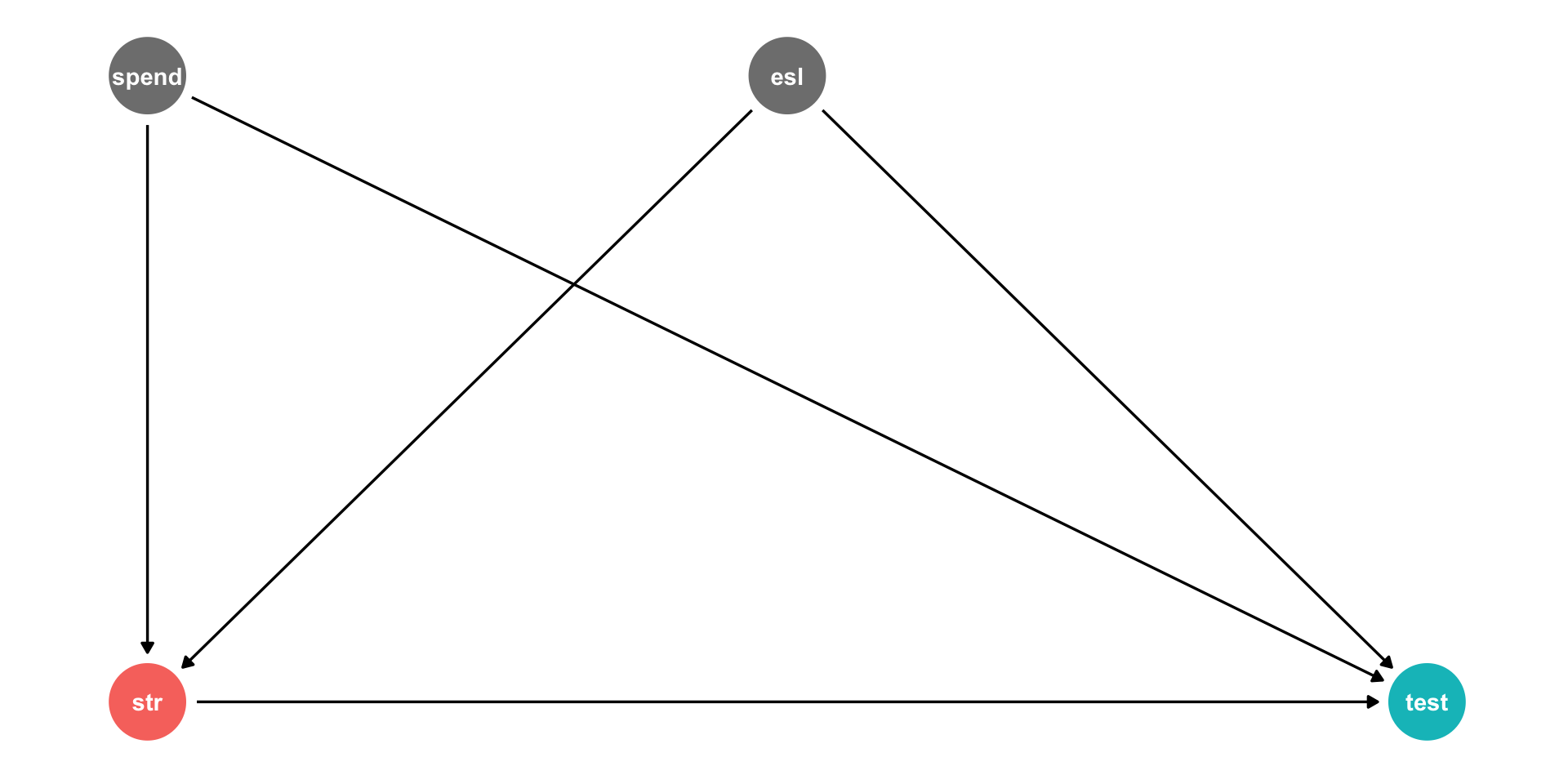

Measuring Omitted Variable Bias I

- Suppose the true population model of a relationship is:

Yi=β0+β1X1i+β2X2i+ui

- What happens when we run a regression and omit X2i?

- Suppose we estimate the following omitted regression of just Yi on X1i (omitting X2i):1

Yi=α0+α1X1i+νi

Measuring Omitted Variable Bias II

- Key Question: are X1i and X2i correlated?

- Run an auxiliary regression of X2i on X1i to see:1

X2i=δ0+δ1X1i+τi

If δ1=0, then X1i and X2i are not linearly related

If |δ1| is very big, then X1i and X2i are strongly linearly related

Measuring Omitted Variable Bias III

- Now substitute our auxiliary regression between X2i and X1i into the true model:

- We know X2i=δ0+δ1X1i+τi

Yi=β0+β1X1i+β2X2i+ui

Measuring Omitted Variable Bias III

- Now substitute our auxiliary regression between X2i and X1i into the true model:

- We know X2i=δ0+δ1X1i+τi

Yi=β0+β1X1i+β2X2i+uiYi=β0+β1X1i+β2(δ0+δ1X1i+τi)+ui

Measuring Omitted Variable Bias III

- Now substitute our auxiliary regression between X2i and X1i into the true model:

- We know X2i=δ0+δ1X1i+τi

Yi=β0+β1X1i+β2X2i+uiYi=β0+β1X1i+β2(δ0+δ1X1i+τi)+uiYi=(β0+β2δ0)+(β1+β2δ1)X1i+(β2τi+ui)

Measuring Omitted Variable Bias III

- Now substitute our auxiliary regression between X2i and X1i into the true model:

- We know X2i=δ0+δ1X1i+τi

Yi=β0+β1X1i+β2X2i+uiYi=β0+β1X1i+β2(δ0+δ1X1i+τi)+uiYi=(β0+β2δ0⏟α0)+(β1+β2δ1⏟α1)X1i+(β2τi+ui⏟νi)

- Now relabel each of the three terms as the OLS estimates (α’s) and error (νi) from the omitted regression, so we again have:

Yi=α0+α1X1i+νi

- Crucially, this means that our OLS estimate for X1i in the omitted regression is:

α1=β1+β2δ1

Measuring Omitted Variable Bias IV

α1=β1+β2δ1

- The Omitted Regression OLS estimate for X1, (α1) picks up both:

- The true effect of X1 on Y: β1

- The true effect of X2 on Y: β2…as pulled through the relationship between X1 and X2: δ1

- Recall our conditions for omitted variable bias from some variable Zi:

- Zi must be a determinant of Yi ⟹ β2≠0

- Zi must be correlated with Xi ⟹ δ1≠0

- Otherwise, if Zi does not fit these conditions, α1=β1 and the omitted regression is unbiased!

Measuring OVB in Our Class Size Example I

- The “True” Regression (Yi on X1i and X2i)

^Test Scorei=686.03−1.10 STRi−0.65 %ELi

| ABCDEFGHIJ0123456789 |

term <chr> | estimate <dbl> | std.error <dbl> | statistic <dbl> | p.value <dbl> |

|---|---|---|---|---|

| (Intercept) | 686.0322487 | 7.41131248 | 92.565554 | 3.871501e-280 |

| str | -1.1012959 | 0.38027832 | -2.896026 | 3.978056e-03 |

| el_pct | -0.6497768 | 0.03934255 | -16.515879 | 1.657506e-47 |

3 rows

Measuring OVB in Our Class Size Example II

- The “Omitted” Regression (Yi on just X1i)

^Test Scorei=698.93−2.28 STRi

| ABCDEFGHIJ0123456789 |

term <chr> | estimate <dbl> | std.error <dbl> | statistic <dbl> | p.value <dbl> |

|---|---|---|---|---|

| (Intercept) | 698.932952 | 9.4674914 | 73.824514 | 6.569925e-242 |

| str | -2.279808 | 0.4798256 | -4.751327 | 2.783307e-06 |

2 rows

Measuring OVB in Our Class Size Example III

- The “Auxiliary” Regression (X2i on X1i)

^%ELi=−19.85+1.81 STRi

| ABCDEFGHIJ0123456789 |

term <chr> | estimate <dbl> | std.error <dbl> | statistic <dbl> | p.value <dbl> |

|---|---|---|---|---|

| (Intercept) | -19.854055 | 9.1626044 | -2.166857 | 0.0308099863 |

| str | 1.813719 | 0.4643735 | 3.905733 | 0.0001095165 |

2 rows

Measuring OVB in Our Class Size Example IV

“True” Regression

^Test Scorei=686.03−1.10 STRi−0.65 %EL

“Omitted” Regression

^Test Scorei=698.93−2.28 STRi

“Auxiliary” Regression

^%ELi=−19.85+1.81 STRi

- Omitted Regression α1 on STR is -2.28

Measuring OVB in Our Class Size Example IV

“True” Regression

^Test Scorei=686.03−1.10 STRi−0.65 %EL

“Omitted” Regression

^Test Scorei=698.93−2.28 STRi

“Auxiliary” Regression

^%ELi=−19.85+1.81 STRi

- Omitted Regression α1 on STR is -2.28

α1=β1+β2δ1

- The true effect of STR on Test Score: -1.10

Measuring OVB in Our Class Size Example IV

“True” Regression

^Test Scorei=686.03−1.10 STRi−0.65 %EL

“Omitted” Regression

^Test Scorei=698.93−2.28 STRi

“Auxiliary” Regression

^%ELi=−19.85+1.81 STRi

- Omitted Regression α1 on STR is -2.28

α1=β1+β2δ1

The true effect of STR on Test Score: -1.10

The true effect of %EL on Test Score: -0.65

Measuring OVB in Our Class Size Example IV

“True” Regression

^Test Scorei=686.03−1.10 STRi−0.65 %EL

“Omitted” Regression

^Test Scorei=698.93−2.28 STRi

“Auxiliary” Regression

^%ELi=−19.85+1.81 STRi

- Omitted Regression α1 on STR is -2.28

α1=β1+β2δ1

The true effect of STR on Test Score: -1.10

The true effect of %EL on Test Score: -0.65

The relationship between STR and %EL: 1.81

Measuring OVB in Our Class Size Example IV

“True” Regression

^Test Scorei=686.03−1.10 STRi−0.65 %EL

“Omitted” Regression

^Test Scorei=698.93−2.28 STRi

“Auxiliary” Regression

^%ELi=−19.85+1.81 STRi

- Omitted Regression α1 on STR is -2.28

α1=β1+β2δ1

The true effect of STR on Test Score: -1.10

The true effect of %EL on Test Score: -0.65

The relationship between STR and %EL: 1.81

So, for the omitted regression:

−2.28=−1.10+(−0.65)(1.81)

Measuring OVB in Our Class Size Example IV

“True” Regression

^Test Scorei=686.03−1.10 STRi−0.65 %EL

“Omitted” Regression

^Test Scorei=698.93−2.28 STRi

“Auxiliary” Regression

^%ELi=−19.85+1.81 STRi

- Omitted Regression α1 on STR is -2.28

α1=β1+β2δ1

The true effect of STR on Test Score: -1.10

The true effect of %EL on Test Score: -0.65

The relationship between STR and %EL: 1.81

So, for the omitted regression:

−2.28=−1.10+(−0.65)(1.81)⏟O.V.Bias=−1.18

Precision of ^βj

Precision of ^βj I

σ^βj; how precise or uncertain are our estimates?

Variance σ2^βj or standard error σ^βj

Precision of ^βj II

var(^βj)=11−R2j⏟VIF×(SER)2n×var(X)

se(^βj)=√var(^βj)

- Variation in ^βj is affected by four things now1:

- Goodness of fit of the model (SER)

- Larger SER → larger var(^βj)

- Sample size, n

- Larger n → smaller var(^βj)

- Variance of X

- Larger var(X) → smaller var(^βj)

- Variance Inflation Factor 1(1−R2j)

- Larger VIF, larger var(^βj)

- This is the only new effect

VIF and Multicollinearity I

- Two independent (X) variables are multicollinear:

cor(Xj,Xl)≠0∀j≠l

- Multicollinearity between X variables does not bias OLS estimates

- Remember, we pulled another variable out of u into the regression

- If it were omitted, then it would cause omitted variable bias!

- Multicollinearity does increase the variance of each OLS estimator by

VIF=1(1−R2j)

VIF and Multicollinearity II

VIF=1(1−R2j)

- R2j is the R2 from an auxiliary regression of Xj on all other regressors (X’s)

- i.e. proportion of var(Xj) explained by other X’s

VIF and Multicollinearity III

Example

Suppose we have a regression with three regressors (k=3):

Yi=β0+β1X1i+β2X2i+β3X3i+ui

- There will be three different R2j’s, one for each regressor:

R21 for X1i=γ+γX2i+γX3iR22 for X2i=ζ0+ζ1X1i+ζ2X3iR23 for X3i=η0+η1X1i+η2X2i

VIF and Multicollinearity IV

VIF=1(1−R2j)

R2j is the R2 from an auxiliary regression of Xj on all other regressors (X’s)

- i.e. proportion of var(Xj) explained by other X’s

The R2j tells us how much other regressors explain regressor Xj

Key Takeaway: If other X variables explain Xj well (high R2J), it will be harder to tell how cleanly Xj→Yi, and so var(^βj) will be higher

VIF and Multicollinearity V

- Common to calculate the Variance Inflation Factor (VIF) for each regressor:

VIF=1(1−R2j)

- VIF quantifies the factor (scalar) by which var(^βj) increases because of multicollinearity

- e.g. VIF of 2, 3, etc. ⟹ variance increases by 2x, 3x, etc.

- Baseline: R2j=0 ⟹ no multicollinearity ⟹VIF=1 (no inflation)

- Larger R2j ⟹ larger VIF

- Rule of thumb: VIF>10 is problematic

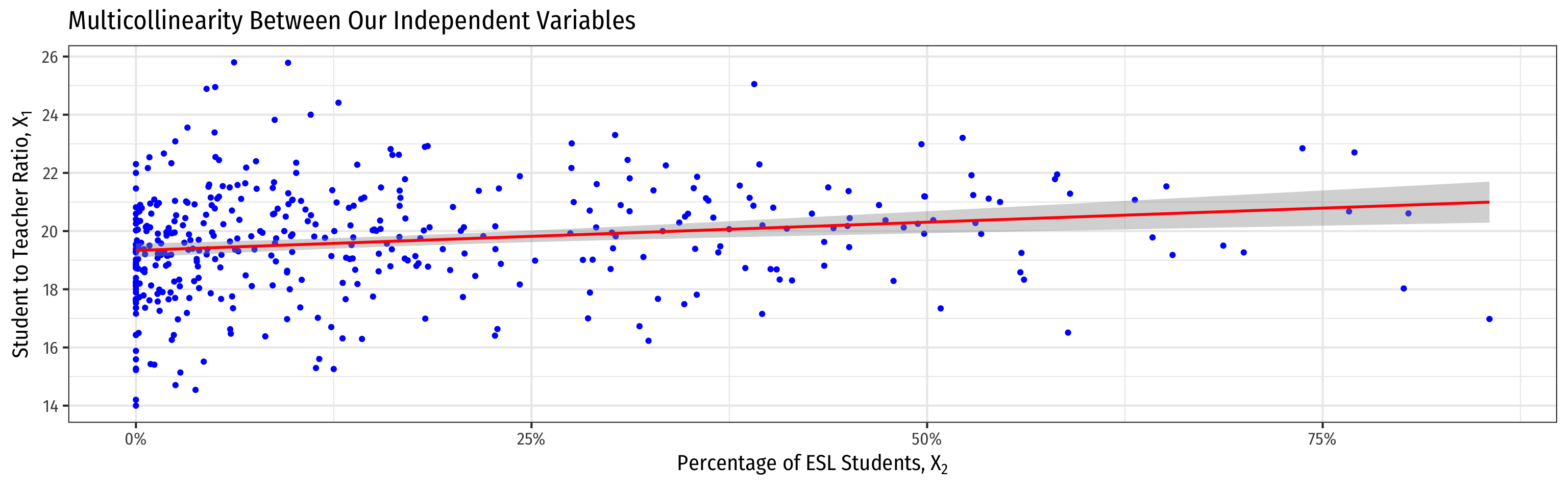

VIF and Multicollinearity in Our Example I

- Higher %EL predicts higher STR

- Hard to get a precise marginal effect of STR holding %EL constant

- Don’t have much data on districts with low STR and high %EL (and vice versa)!

VIF and Multicollinearity in Our Example II

- Again, consider the correlation between the variables

str testscr el_pct

str 1.0000000 -0.2263628 0.1876424

testscr -0.2263628 1.0000000 -0.6441237

el_pct 0.1876424 -0.6441237 1.0000000- cor(STR,%EL)=−0.644

VIF and Multicollinearity in R I

str el_pct

1.036495 1.036495 - var(^β1) on

strincreases by 1.036 times (3.6%) due to multicollinearity withel_pct - var(^β2) on

el_pctincreases by 1.036 times (3.6%) due to multicollinearity withstr

VIF and Multicollinearity in R II

- Let’s calculate VIF manually to see where it comes from:

| ABCDEFGHIJ0123456789 |

term <chr> | estimate <dbl> | std.error <dbl> | statistic <dbl> | p.value <dbl> |

|---|---|---|---|---|

| (Intercept) | -19.854055 | 9.1626044 | -2.166857 | 0.0308099863 |

| str | 1.813719 | 0.4643735 | 3.905733 | 0.0001095165 |

2 rows

VIF and Multicollinearity in R III

VIF and Multicollinearity in R IV

[1] 1.036495- Again, multicollinearity between the two X variables inflates the variance on each by 1.036 times

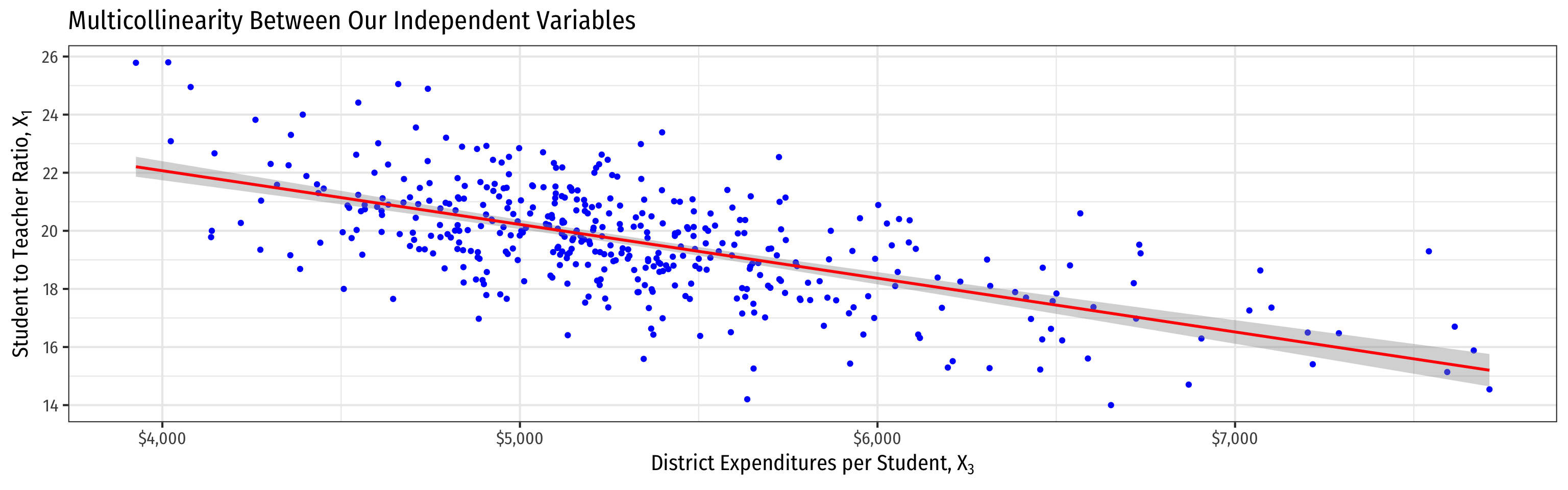

Another Example: Expenditures/Student I

Example

What about district expenditures per student?

Another Example: Expenditures/Student II

- Higher spend predicts lower STR

- Hard to get a precise marginal effect of STR holding spend constant

- Don’t have much data on districts with high STR and high spend (and vice versa)!

Another Example: Expenditures/Student II

Would omitting Expenditures per student cause omitted variable bias?

cor(Test,spend)≠0

cor(STR,spend)≠0

Another Example: Expenditures/Student III

| ABCDEFGHIJ0123456789 |

term <chr> | estimate <dbl> | std.error <dbl> | statistic <dbl> | p.value <dbl> |

|---|---|---|---|---|

| (Intercept) | 649.577947257 | 15.205718554 | 42.7193194 | 3.299149e-154 |

| str | -0.286399240 | 0.480523198 | -0.5960154 | 5.514891e-01 |

| el_pct | -0.656022660 | 0.039105885 | -16.7755481 | 1.295346e-48 |

| expn_stu | 0.003867902 | 0.001412122 | 2.7390698 | 6.426186e-03 |

4 rows

- Including

expn_stureduces bias but increases variance of β1 by 1.68x (68%)- and variance of β2 by 1.04x (4%)

Multicollinearity Increases Variance

| Test Scores | Test Scores | Test Scores | |

|---|---|---|---|

| Constant | 698.93*** | 686.03*** | 649.58*** |

| (9.47) | (7.41) | (15.21) | |

| Student Teacher Ratio | −2.28*** | −1.10*** | −0.29 |

| (0.48) | (0.38) | (0.48) | |

| Percent ESL Students | −0.65*** | −0.66*** | |

| (0.04) | (0.04) | ||

| Spending per Student | 0.00*** | ||

| (0.00) | |||

| n | 420 | 420 | 420 |

| R2 | 0.05 | 0.43 | 0.44 |

| SER | 18.54 | 14.41 | 14.28 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

Perfect Multicollinearity

- Perfect multicollinearity is when a regressor is an exact linear function of (an)other regressor(s)

^Sales=^β0+^β1Temperature (C)+^β2Temperature (F)

Temperature (F)=32+1.8∗Temperature (C)

- cor(temperature (F), temperature (C))=1

- R2j=1→VIF=11−1→var(^βj)=0!

- This is fatal for a regression

- A logical impossiblity, always caused by human error

Perfect Multicollinearity: Example

Example

^TestScorei=^β0+^β1STRi+^β2%EL+^β3%EF

%EL: the percentage of students learning English

%EF: the percentage of students fluent in English

%EF=100−%EL

|cor(%EF,%EL)|=1

Perfect Multicollinearity: Example II

| ABCDEFGHIJ0123456789 |

cor <dbl> |

|---|

| -1 |

1 row

Perfect Multicollinearity: Example III

Perfect Multicollinearity Example IV

Call:

lm(formula = testscr ~ str + el_pct + ef_pct, data = ca_school_ex)

Residuals:

Min 1Q Median 3Q Max

-48.845 -10.240 -0.308 9.815 43.461

Coefficients: (1 not defined because of singularities)

Estimate Std. Error t value Pr(>|t|)

(Intercept) 686.03225 7.41131 92.566 < 2e-16 ***

str -1.10130 0.38028 -2.896 0.00398 **

el_pct -0.64978 0.03934 -16.516 < 2e-16 ***

ef_pct NA NA NA NA

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 14.46 on 417 degrees of freedom

Multiple R-squared: 0.4264, Adjusted R-squared: 0.4237

F-statistic: 155 on 2 and 417 DF, p-value: < 2.2e-16- Note

Rdrops one of the multicollinear regressors (ef_pct) if you include both 🤡

A Summary of Multivariate OLS Estimator Properties

A Summary of Multivariate OLS Estimator Properties

- ^βj on Xj is biased only if there is an omitted variable (Z) such that:

- cor(Y,Z)≠0

- cor(Xj,Z)≠0

- If Z is included and Xj is collinear with Z, this does not cause a bias

- var[^βj] and se[^βj] measure precision (or uncertainty) of estimate:

var[^βj]=1(1−R2j)∗SER2n×var[Xj]

- VIF from multicollinearity: 1(1−R2j)

- R2j for auxiliary regression of Xj on all other X’s

- mutlicollinearity does not bias ^βj but raises its variance

- perfect multicollinearity if X’s are linear function of others

(Updated) Measures of Fit

(Updated) Measures of Fit

Again, how well does a linear model fit the data?

How much variation in Yi is “explained” by variation in the model (^Yi)?

Yi=^Yi+^ui^ui=Yi−^Yi

(Updated) Measures of Fit: SER

- Again, the Standard errror of the regression (SER) estimates the standard error of u

SER=SSRn−k−1

A measure of the spread of the observations around the regression line (in units of Y), the average “size” of the residual

Only new change: divided by n−k−1 due to use of k+1 degrees of freedom to first estimate β0 and then all of the other β’s for the k number of regressors1

(Updated) Measures of Fit: R2

R2=SSMSST=1−SSRSST=(rX,Y)2

- Again, R2 is fraction of total variation in Yi (“total sum of squares”) that is explained by variation in predicted values (^Yi), i.e. our model (“model sum of squares”)

R2=var(ˆY)var(Y)

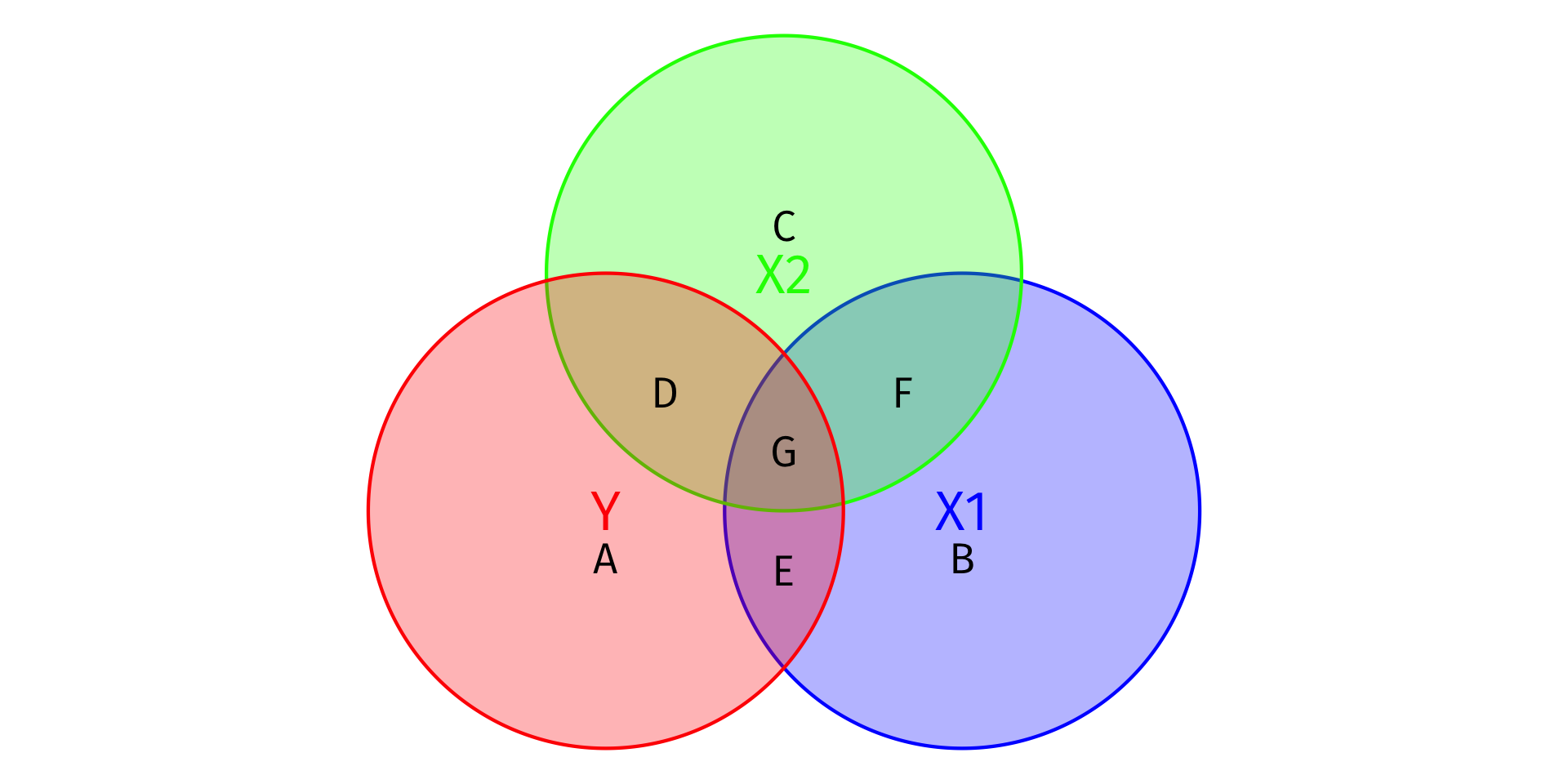

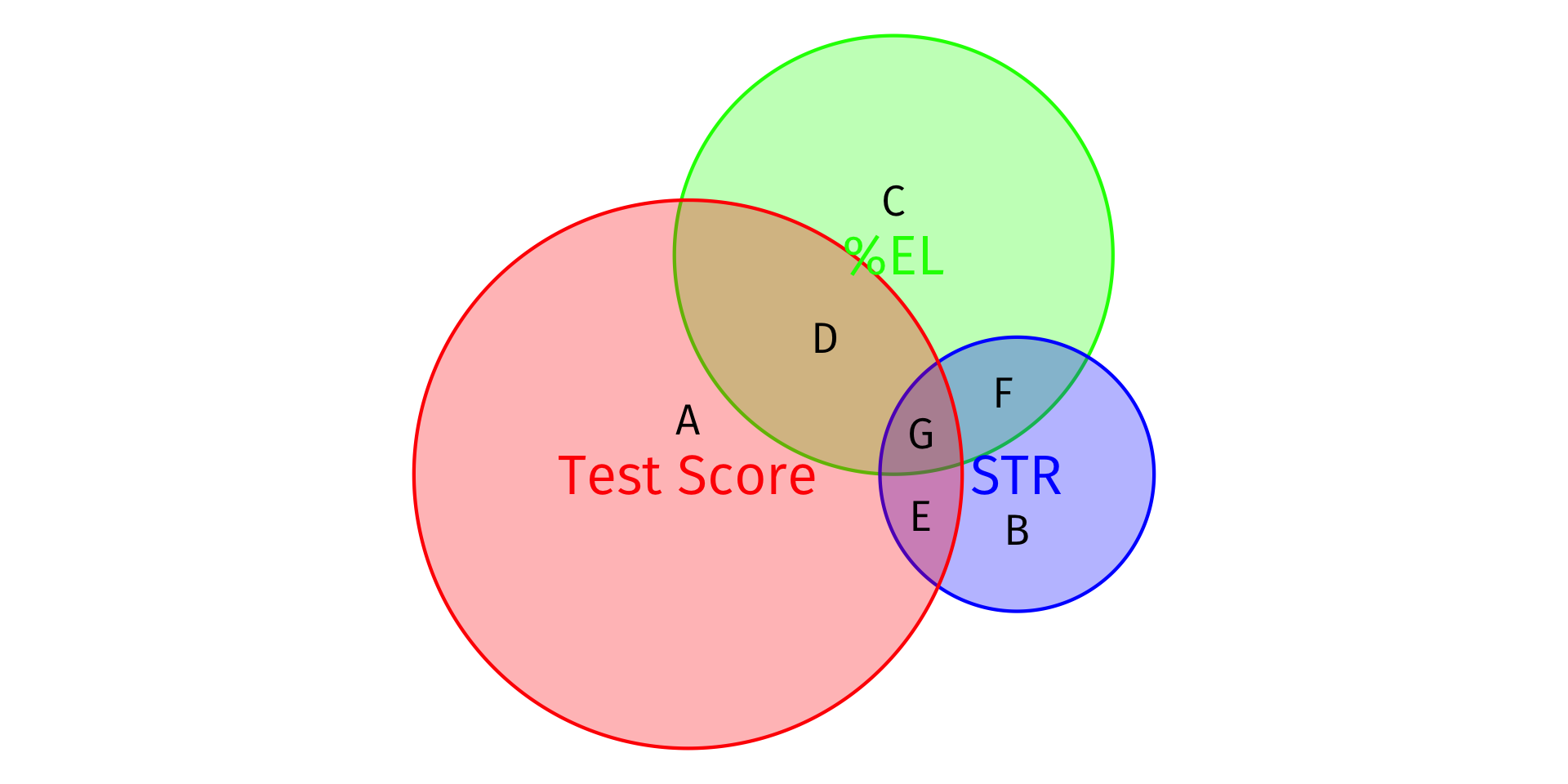

Visualizing R2

- Total Variation in Y: Areas A + D + E + G

SST=n∑i=1(Yi−ˉY)2

- Variation in Y explained by X1 and X2: Areas D + E + G

SSM=n∑i=1(^Yi−ˉY)2

- Unexplained variation in Y: Area A

SSR=n∑i=1(^ui)2

R2=SSMSST=D+E+GA+D+E+G

Visualizing R2

# make a function to calc. sum of sq. devs

sum_sq <- function(x){sum((x - mean(x))^2)}

# find total sum of squares

SST <- elreg %>%

augment() %>%

summarize(SST = sum_sq(testscr))

# find explained sum of squares

SSM <- elreg %>%

augment() %>%

summarize(SSM = sum_sq(.fitted))

# look at them and divide to get R^2

tribble(

~SSM, ~SST, ~R_sq,

SSM, SST, SSM/SST

) %>%

knitr::kable()| SSM | SST | R_sq |

|---|---|---|

| 64864.3 | 152109.6 | 0.4264314 |

R2=SSMSST=D+E+GA+D+E+G

(Updated) Measures of Fit: Adjusted ˉR2

- Problem: R2 mechanically increases every time a new variable is added (it reduces SSR!)

- Think in the diagram: more area of Y covered by more X variables!

- This does not mean adding a variable improves the fit of the model per se, R2 gets inflated

- We correct for this effect with the adjusted ˉR2 which penalizes adding new variables:

ˉR2=1−n−1n−k−1⏟penalty×SSRSST

- In the end, recall R2 was never that useful1, so don’t worry about the formula

- Large sample sizes (n) make R2 and ˉR2 very close

ˉR2 In R

Call:

lm(formula = testscr ~ str + el_pct, data = ca_school)

Residuals:

Min 1Q Median 3Q Max

-48.845 -10.240 -0.308 9.815 43.461

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 686.03225 7.41131 92.566 < 2e-16 ***

str -1.10130 0.38028 -2.896 0.00398 **

el_pct -0.64978 0.03934 -16.516 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 14.46 on 417 degrees of freedom

Multiple R-squared: 0.4264, Adjusted R-squared: 0.4237

F-statistic: 155 on 2 and 417 DF, p-value: < 2.2e-16- Base R2 (

Rcalls it “Multiple R-squared”) went up Adjusted R-squared(ˉR2) went down

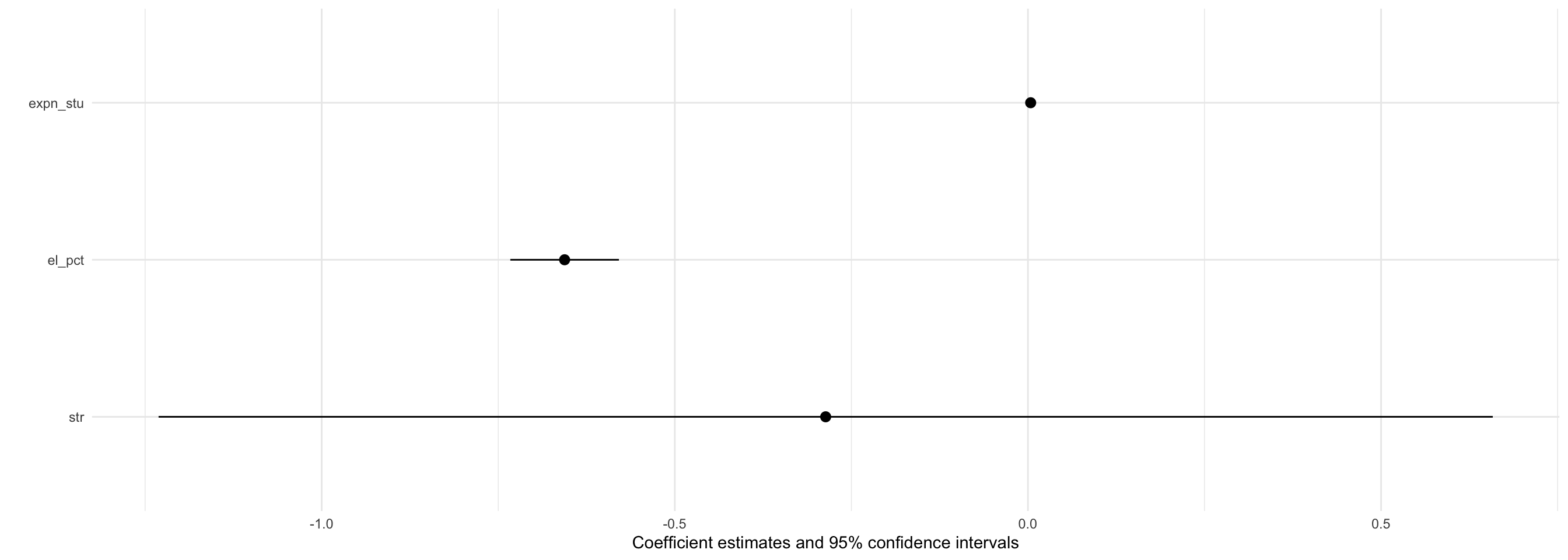

Coefficient Plots (with modelsummary)

Regression Table (with modelsummary)

| Simple Model | MV Model 1 | MV Model 2 | |

|---|---|---|---|

| Constant | 698.93*** | 686.03*** | 649.58*** |

| (9.47) | (7.41) | (15.21) | |

| STR | −2.28*** | −1.10*** | −0.29 |

| (0.48) | (0.38) | (0.48) | |

| % ESL Students | −0.65*** | −0.66*** | |

| (0.04) | (0.04) | ||

| Spending per Student | 0.00*** | ||

| (0.00) | |||

| N | 420 | 420 | 420 |

| Adj. R2 | 0.05 | 0.42 | 0.43 |

| SER | 18.54 | 14.41 | 14.28 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

modelsummary(models = list("Simple Model" = school_reg,

"MV Model 1" = elreg,

"MV Model 2" = reg3),

fmt = 2, # round to 2 decimals

output = "html",

coef_rename = c("(Intercept)" = "Constant",

"str" = "STR",

"el_pct" = "% ESL Students",

"expn_stu" = "Spending per Student"),

gof_map = list(

list("raw" = "nobs", "clean" = "N", "fmt" = 0),

#list("raw" = "r.squared", "clean" = "R<sup>2</sup>", "fmt" = 2),

list("raw" = "adj.r.squared", "clean" = "Adj. R<sup>2</sup>", "fmt" = 2),

list("raw" = "rmse", "clean" = "SER", "fmt" = 2)

),

escape = FALSE,

stars = c('*' = .1, '**' = .05, '***' = 0.01)

)

4.1 — Multivariate OLS Estimators ECON 480 • Econometrics • Fall 2022 Dr. Ryan Safner Associate Professor of Economics safner@hood.edu ryansafner/metricsF22 metricsF22.classes.ryansafner.com